Home • Articles • Why I think Cash Lifetime ISAs are better than Help to Buy ISAs when saving for a home

Why I think Cash Lifetime ISAs are better than Help to Buy ISAs when saving for a home

13 Dec, 2018

When I tell people that I’ve chosen to save for my future home by opening up a Cash Lifetime ISA, it’s almost 50:50 what the reaction will be. Rather like Marmite or Bruce Forsyth, it seems that Cash LISAs are somewhat polarising...

Phoebe Smith of Boring Money presents the case for Cash LISAs

As a university graduate with a massive chunk of student debt, I’m only too aware of the gloomy headlines proclaiming exponentially rising house prices, and the apocalyptic wasteland forecast for our post-Brexit economy. So I’m understandably enticed by any edge I can get when scrabbling onto the property ladder.

I’ve heard various arguments against the Cash LISA which range from its impracticability as a home-buying tool to its flaws as a retirement pot:

- “They are unnecessarily complicated, with the potential that many will have been mis-sold one. For most people the only benefit is if you are absolutely certain you are going to use it to buy a property, which is becoming increasingly difficult in the current housing market!”

- “If you end up not buying a property, it has a withdrawal penalty of 25% if you take money out before the age of 60! In comparison you only lose the government bonus in a Help to Buy ISA, and you keep the good interest rates that come with it (currently 2.58% with Barclays)”

- “If you end up using the savings for retirement, most people would have been better off with a pension due to benefits such as employer contributions, tax relief, potential investment gains over the long term, and the ability to withdraw it at 55 (currently), rather than 60!”

These arguments - coupled with the fact that until August this year, there was just one Cash Lifetime ISA on the market (thanks Skipton!) - hardly encourage prospective new homeowners to shun the Help to Buy ISA, in favour of its lesser-known cousin.

However, since August 2018, two new Cash LISAs have sprung up from both Nottingham and Newcastle Building Societies, and it seems that Cash LISAs are finally getting the love I think they deserve.

Meanwhile, Help to Buy ISAs seem to be on the decline. They will not be available to new savers after 30th November 2019, and it will only be possible to get the government bonus for a deposit until 2030.

So, what’s the difference between a Cash Lifetime ISA and a Help to Buy ISA?

They’re pretty similar sounding propositions on the surface, but there are some big distinctions.

Let’s take a look at those differences...

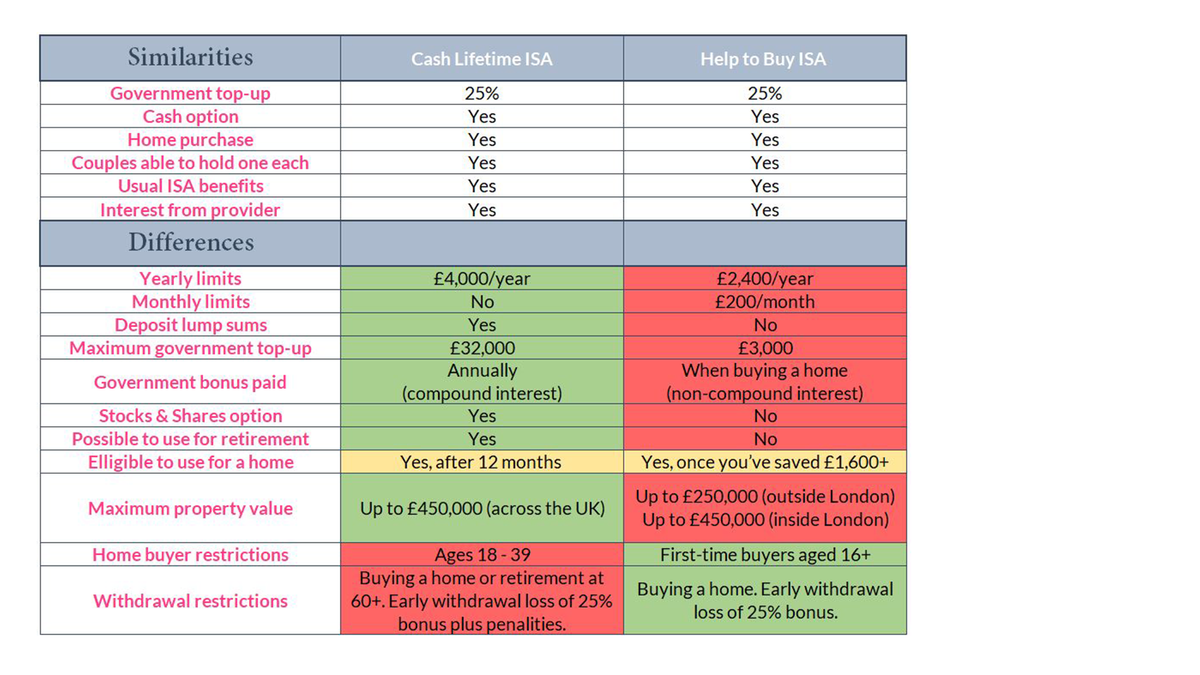

Yearly limits

Cash LISA – you can save up to £4,000 a year

Help to Buy ISA – you can save up to £2,400 a year (up to £3,400 in year one), with a limit of £200 per month

With a higher yearly limit, saving up with a Cash LISA can be faster. Plus, a £200 per month limit for Help to Buy ISAs doesn’t allow you to offset lean months when you can’t save, by increasing your monthly savings later in the year.

Lump sum deposits

Cash LISA – you can deposit lump sums

Help to Buy ISA – you can’t deposit lump sums

Some people are lucky enough to experience lump sum windfalls. Maybe a well-placed flutter on the horses, a bonus at work, a tax rebate (haha…) or money from relatives. A ban on lump sum deposits in Help to Buy ISAs is inflexible and inconvenient.

Maximum government top-up

Cash LISA – maximum government top-up is £32,000 (this is if you open it at 18 and pay in the max £4,000 a year over the next 32 years, until the government’s final 25% top up when you turn 50)

Help to Buy ISA – maximum government top-up is £3,000 (after you’ve contributed £12,000, the government will cease to give their 25% top up)

While I’m not one to turn my nose up at free money, a £3,000 cap on the government top-up with a Help to Buy ISA is a mere drop in the ocean when it comes to saving for a house.

It’s easier if you buy as part of a couple with a Help to Buy ISA each. However, a Cash LISA gives savers an opportunity to avoid reliance on a partner when buying a home. And the top-up can be ten times more!

Government bonus paid

• Cash LISA - government bonus paid annually

• Help to Buy ISA - government bonus paid when you buy your home

If your bonus is paid annually, you can also benefit by earning interest on it every year that follows. And then you earn interest on that interest. And so on and so on. This is called compounding, which basically means more free money. Cash LISA wins again!

Stocks & Shares options

Cash LISA – Stocks & Shares options available

Help to Buy ISA – only Cash options available

This is really an argument between guaranteed small returns vs unreliable potentially larger returns. If you’re looking to buy within the next 5 to 10 years, tying the money for your first home into the rise and fall of the stock market feels needlessly risky. However, over a 10 to 15 year period you might be more likely to see your money grow.

Possible to use for retirement?

Cash LISA – yes, can be used for retirement from the age of 60

Help to Buy ISA – no, it can only be used for a first home

Once again, the Cash LISA proves itself to be more flexible. However, I do agree with the argument that for anyone with an employer, a Cash LISA is not the best option as a retirement pot.

When can you use it for a home?

Cash LISA – can be used to buy a home after it’s been open for 12 months

Help to Buy ISA – can be used to buy a home once you’ve saved over £1,600

Here again, there’s no clear winner.

If you are looking to buy within the next 12 months, a Cash LISA is not for you. However, with the Help to Buy ISA’s monthly £200 cap, after 12 months of savings (and assuming you make use of the higher £1,200 monthly cap in the first month) you’ll only have £3,400 saved. Which is better than nothing, but not much to put towards buying a house.

Maximum property value

Cash LISA – can be used for a property of up to £450,000

Help to Buy ISA – can be used for a property of up to £250,000 (up to £450,000 in London)

And again I say, the Cash LISA is more flexible, with its higher £450,000 cap across the UK. The Help to Buy ISA’s £250,000 cap outside of London is pretty restrictive, possibly pushing first-time buyers into purchasing houses in locations far from their workplace and family, or smaller than their needs. This may seem picky, but a greater amount of flexibility in choosing where to live is a huge comfort. No one wants to uproot their whole life due to the cap on their Help to Buy ISA.

Home buyer restrictions

Cash LISA – Only available to people aged 18 to 39

Help to Buy ISA – Available to any first-time buyer aged 16+

The Help to Buy ISA wins this one. It’s much more flexible and allows everyone from school children to pensioners to more easily save for their first home.

Withdrawal restrictions

Cash LISA – when buying a home or for retirement at 60+. If you withdraw earlier, you’ll lose your government bonus, any growth in that contribution, and may pay a 5% surcharge.

Help to Buy ISA – only when buying your first home. If you withdraw earlier, you’ll only lose your government bonus.

While the Cash LISA allows for either first-home or retirement withdrawal, the early withdrawal penalties aren’t great! So you need to be certain that you’ll use the Cash LISA for a first-time home or retirement, so you don’t face the hefty early withdrawal charges.