Home • Articles • The Ultimate Guide to Inheritance Tax in the UK: Allowances, Exemptions and Planning Tips

The Ultimate Guide to Inheritance Tax in the UK: Allowances, Exemptions and Planning Tips

By Boring Money

20 June, 2025

The basics of Inheritance Tax

Inheritance Tax (IHT) is a tax on the estate

(that’s property, money and possessions) of someone who has died. Most people don’t end up paying it because of tax-free allowances. But if your estate exceeds a certain amount, HMRC may want a slice, which can land your loved ones with a hefty tax bill when you're no longer around.How much is Inheritance Tax?

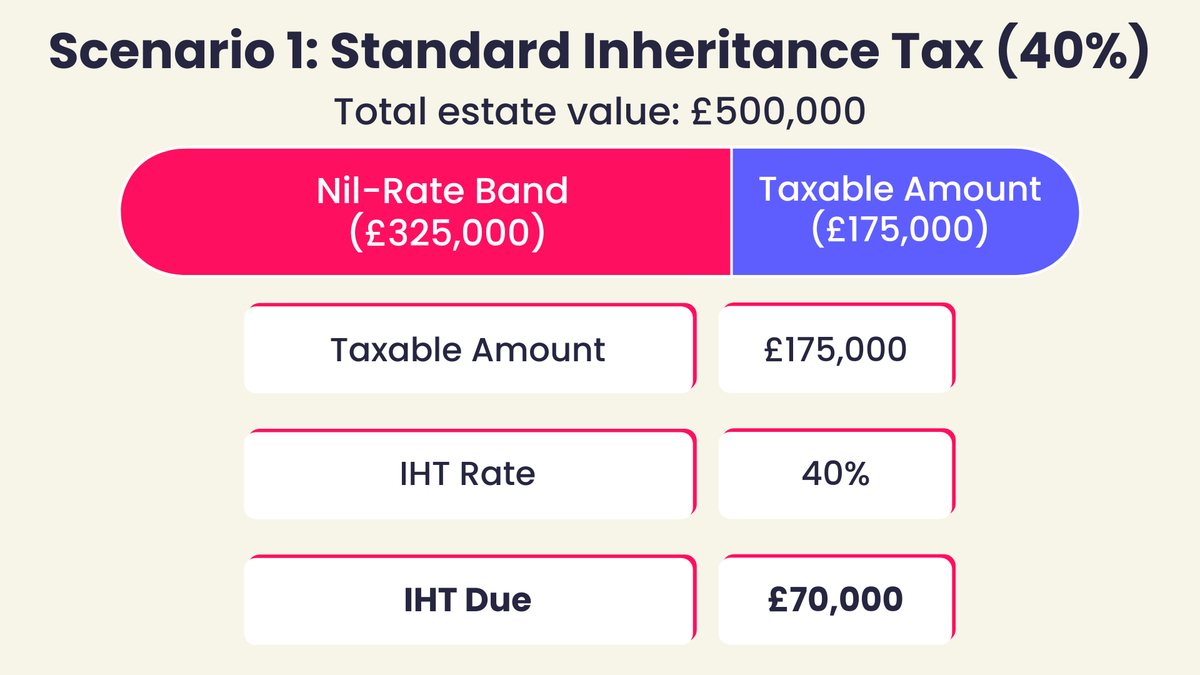

Standard IHT rate

Inheritance Tax is currently charged at 40% on the amount above the £325,000 threshold - this is known as the nil-rate band (NRB). Everything under that = no tax. Anything over = HMRC swoops in.

For illustrative purposes only.

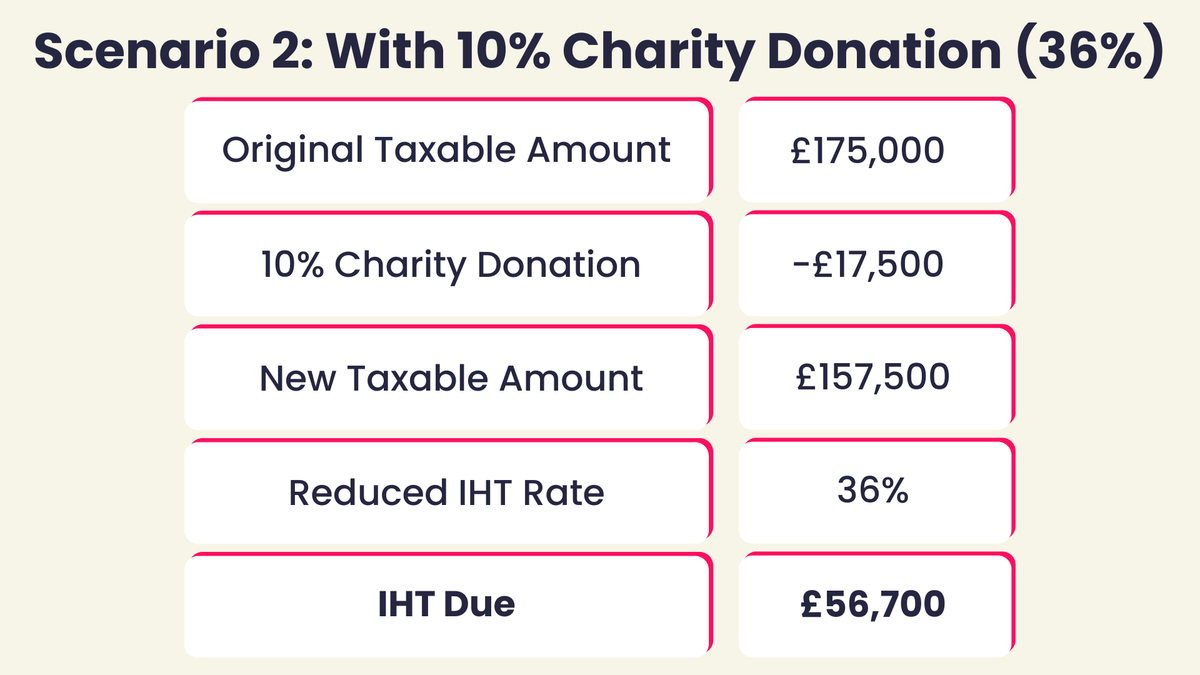

Reduced IHT rate

It's possible to reduce the rate of Inheritance Tax due on your estate if you're feeling generous. If you leave at least 10% of the value of your estate to charity, your IHT rate will be reduced to 36% (rather than the headline 40%).

For illustrative purposes only.

When does Inheritance Tax not apply?

Good news: just because someone dies doesn’t mean HMRC automatically gets a cut. There are several common situations where Inheritance Tax simply doesn’t apply at all, including:

If your estate is worth £325,000 or less, there’s no Inheritance Tax to pay. This is called the nil-rate band. Remember if you’re leaving your main residence to children or grandchildren, you may also qualify for the residence nil-rate band, which boosts your allowance up to £500,000 (or up to £1 million for couples).

Transfers between spouses or civil partners are completely exempt from Inheritance Tax - no matter how much you pass on. Even better, any unused allowance from the first partner to die can be transferred to the surviving spouse. Therefore the basic tax-free allowance can be as much as £650,000 if none of the £325,000 threshold was used when the first partner of the couple died.

If you leave your estate to a UK-registered charity, that part is tax-free. And if you donate 10% or more of your total estate to charity, the IHT rate on the rest drops from 40% to 36%. A win for the cause and for your family.

Gifts made during your lifetime are generally exempt from IHT if you survive for at least seven years afterwards. This is known as the 7 Year Rule (more on this below). You can also give away smaller gifts - up to £3,000 in total per year - that are always exempt, regardless of when you die.

Who pays Inheritance Tax?

Technically, your estate pays the Inheritance Tax bill before anything is passed on - so your loved ones don't have to go scrambling around in their own pockets.

Since IHT is only payable once you’ve passed away, it usually falls to the executor of your will

to arrange paying the tax out of your estate. If you don’t have a will in place when you die, it’s the administrator of your estate who has this responsibility.Most of the time, Inheritance Tax is paid through the Direct Payment Scheme (DPS). If you have money in a bank or building society account when you die, whoever’s in charge of your estate can ask for some (or all) of the amount due to be paid to be transferred directly from the account to the government.

IHT on gifts given in the seven years leading up to your death must be paid by the recipient (but more on this later).

What happens if there is no cash in the estate?

If your estate contains assets liable for IHT but little or no cash to cover the bill, the administrator must find a way to release funds in order to pay it. There are a number of ways to do this, including:

Instalment payments: IHT on property and certain business assets can be paid in instalments over a 10-year period, with the first instalment due before probate

is granted. Interest is then charged on the outstanding balance (see next section for details).Executor or beneficiary loans: The executor of your will or a beneficiary may pay the IHT out of their own funds and then reclaim it from the estate once the assets of equivalent value have been sold or distributed.

Bridging loans: Executors can take out short-term loans secured against the estate’s assets to pay the IHT.

Grant on credit: In exceptional cases, if other options are not available, HMRC may allow a “grant on credit,” permitting probate to be granted before full tax bill is received (with the tax paid as soon as possible, e.g., after selling a property).

When do you have to pay Inheritance Tax?

The bill is due six months after the end of the month in which the person died - regardless of whether or not you have been granted probate

.HMRC will start charging interest if the payment isn’t made in full and on time. Sometimes Inheritance Tax can be paid in instalments over 10 years, but the government will continue to charge interest on the outstanding amount until the debt is cleared.

The current interest rate is 8.25% as at the 2025-26 tax year. You can use HMRC's IHT interest rate calculator to get an estimate of how much this would cost in your specific scenario.

What gifts are exempt from Inheritance Tax?

Each tax year, you can give away up to £3,000 without it being counted towards your estate for Inheritance Tax purposes. This is known as your annual exemption, but there are other allowances and exemptions which you can utilise when passing on assets or wealth:

You can:

Give £3,000 to one person

Split £3,000 between multiple people

Carry forward unused amount for one year only

You can:

Give £250 to unlimited people

Give birthday/Christmas gifts from your regular income

You cannot:

Combine with other allowances for same person

You can give:

£5,000 to a child

£2,500 to a grandchild/great-grandchild

£1,000 to any other person

Combine with annual exemption

You can:

Make unlimited regular payments from regular income

Must be affordable after usual expenses

Combine with annual exemption

You can give unlimited amounts to:

Your spouse/civil partner (as long as they're a UK resident)

Charities

Political parties

The person giving the gifts should keep thorough records, as the individual dealing with your estate will need to work out what gifts you gave within the seven years leading up to your death (more on this below).

Using the various exemptions and allowances can be a simple, effective way to reduce the size of your estate over time and potentially cut your IHT bill without having to worry about the 7 Year Rule.

What is the 7 Year Rule?

The 7 Year Rule applies to gifts you give during your lifetime. Known as Potentially Exempt Transfers (PETs), they can be completely tax-free as long as you live for seven years after making them. If you die within seven years, the gift may be subject to Inheritance Tax. In that case, it’s usually the person who received the gift who has to pay the tax.

PETs are treated as tax-free when you make them, and provided you survive for seven years after making the gift, no Inheritance Tax is payable. If tax does become due on a PET, the person who received the PET will be asked to pay the tax.

Gifts to your spouse or civil partner

No tax, ever. These are exempt from IHT regardless of when you give them.

Gifts to anyone else

They could be taxed, but the amount depends on how long you survive after making the gift. This is where taper relief kicks in. The longer you live, the less tax is due:

Inheritance Tax taper rate

Years before death | Inheritance Tax due (% of value of gift) |

0-3 | 40% |

3-4 | 32% |

4-5 | 24% |

5-6 | 16% |

6-7 | 8% |

7 or more | 0% |

Key takeaways on Inheritance Tax

💰 Not just for the ultra-wealthy

A lot of people assume Inheritance Tax is only something the very rich have to worry about - but thanks to soaring house prices and frozen thresholds, that’s no longer true. If you own a property, especially in the South East, your estate could easily tip over the nil-rate band (especially if you're unmarried). Add in savings, investments, and personal belongings, and suddenly your estate might be in IHT territory without you realising.

🗓️ Planning ahead can save thousands

Inheritance Tax is one of the few taxes you can genuinely plan your way around. By making use of gift allowances, writing a clear will, and making plans well in advance, you can reduce how much of your estate is exposed to tax. Start early enough and you can also use the 7 Year Rule to pass on larger amounts tax-free - but leave it too late and your options shrink fast.

💡 Know your thresholds and exemptions

There are a range of exemptions and reliefs - from the annual gifting allowance to charity donations - that can make a big difference. Understanding and using them properly is key to keeping more money in the family and out of HMRC’s hands. If in doubt about how to navigate this, a financial adviser can help to assess your estate and draw up a plan to minimise your IHT bill for you.