‘Ready-made’ investment solutions reviews

By Mike Narouei, Content Producer at Boring Money

15 Jan, 2020

Trying to work out which investment providers have performed well after fees is no easy task. After much frustration and endless Excel spreadsheets, we decided that the easiest and least controversial way to measure who does well was simply to open an account, stick £500 in and see how they did. Here is our January 2020 independent guide for consumers.

We opened 19 accounts in the first week of January 2018, buying a ‘medium risk’ investment fund or portfolio with an initial investment of £500. Now of course in practice, interpretations of what is ‘medium risk’ differ. The closest we can come to comparing like with like is to measure collections of investments which have as close to 60% in shares as possible.

So how have they done?

After all fees on the £500 portfolios, the top 5 performers over the 2 year period were the following. We show what the £500 was worth on the day of reckoning, which was 2nd January 2020.

AJ Bell Youinvest - £554

MoneyFarm - £551

Vanguard - £548

Wealthsimple - £547

IG - £547

The numbers represent what is left in the investor account after performance and charges.

The lowest five performing investment options, net of all charges, of those investment platforms offering their branded funds or portfolios were:

Barclays Smart Investor - £434

Fidelity - £444

The Share Centre - £459

Hargreaves Lansdown - £506

Charles Stanley Direct - £510

Before you rush to judge...

Barclays, Fidelity and The Share Centre all have minimum monthly fees or an element of fixed £ fees so it is not fair to look at the above without referencing this. These relatively high charges on our small £500 accounts will of course eat into the balance.

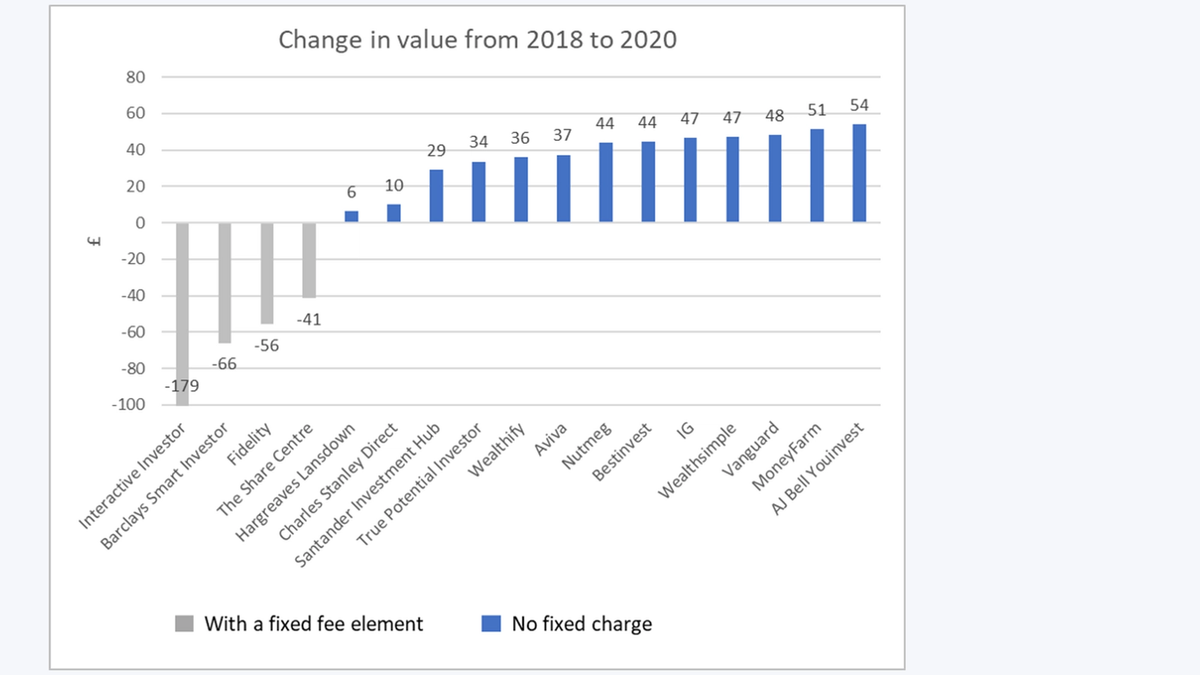

The chart below shows what we made or lost over the last 2 years, after all charges have been deducted.

Notes: As this is a £500 account for illustrative purposes, those platforms with a fixed fee element or a monthly minimum look disproportionately poor and are highlighted here in grey. We include Interactive Investor for comparison – as they do not have proprietary funds, we used the Vanguard LifeStrategy 60% fund and bought this on the II platform.

The contributing factors to any relative and short-term underperformance were charging structures (Fidelity and Barclays both have minimum £ monthly charges which impacts a £500 account), fees (The Share Centre and Hargreaves Lansdown have ongoing fund charges of 1.56% and 1.43% respectively which are much heftier than the ‘passive’ robo advisers ) and asset allocation (Charles Stanley Direct had just 44% in shares in a year when global stock markets typically did well. So a conservative chunk in shares gives the portfolio less oomph).

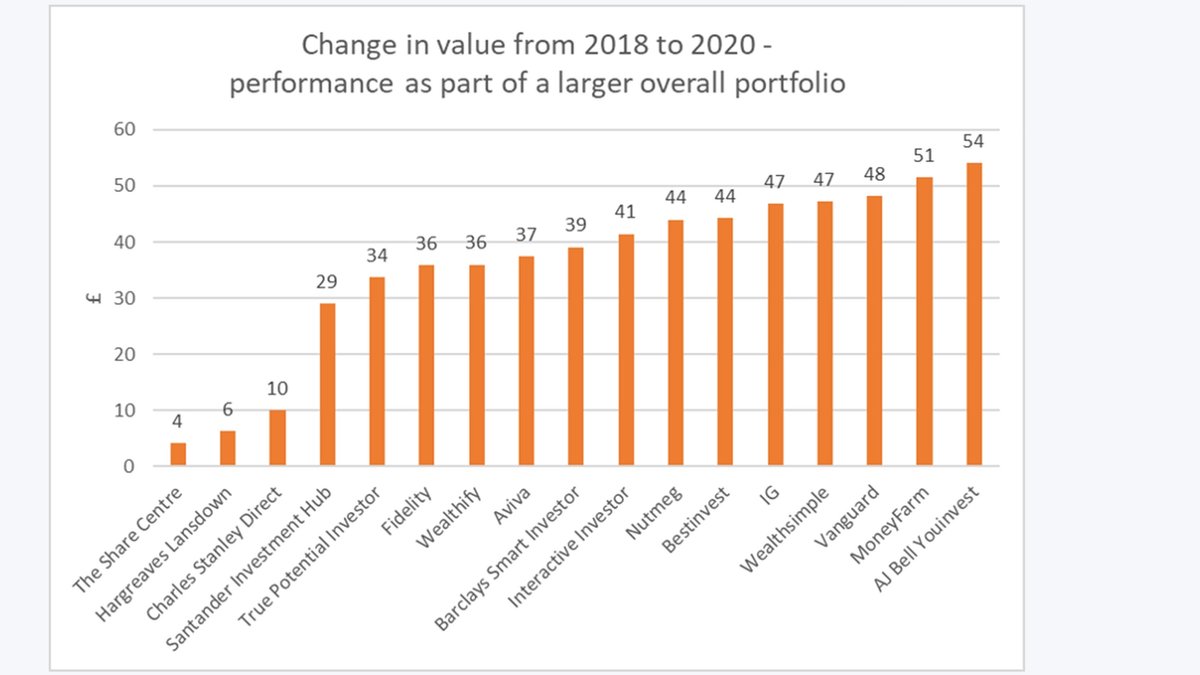

A fairer way to look at performance for those with total sums of £50,000 or more…

The below is arguably a fairer way of illustrating performance, removing the fixed fee versus the % fee argument from the table for a second. If we assume that the £500 fund or portfolio was held as part of a bigger £50,000 investment account, this of course dilutes the blow of any fixed fees or monthly minimums.

For example, Barclays has a £4 a month minimum fee which sounds pretty reasonable, but takes a huge bite out of a £500 account every month! Looking at this as part of a £50,000 portfolio, the impact of this minimum monthly charge disappears and we see the Barclays relative performance look much healthier.

Forget all that being fair stuff, what actually happened to your £500?

OK. Here’s what was left in the accounts after charges on our £500 investment.

The higher the % of shares, the more volatile you’d expect these portfolios to be. So also think about risk. Certain providers might have got you from A to B faster over the last few years, but if they’ve driven at 120 mph on the way, are you comfortable with that? If the shares %s creep up from 60%, some may find that too risky and this can of course backfire when global shares have a meltdown.

So don’t just pick on how providers have done over the last 2 years. Pick the blend of shares which feels right for you too. Lots of the options covered here have free ‘risk profilers’ online which will help you work out what your ideal % allocation to shares might be.

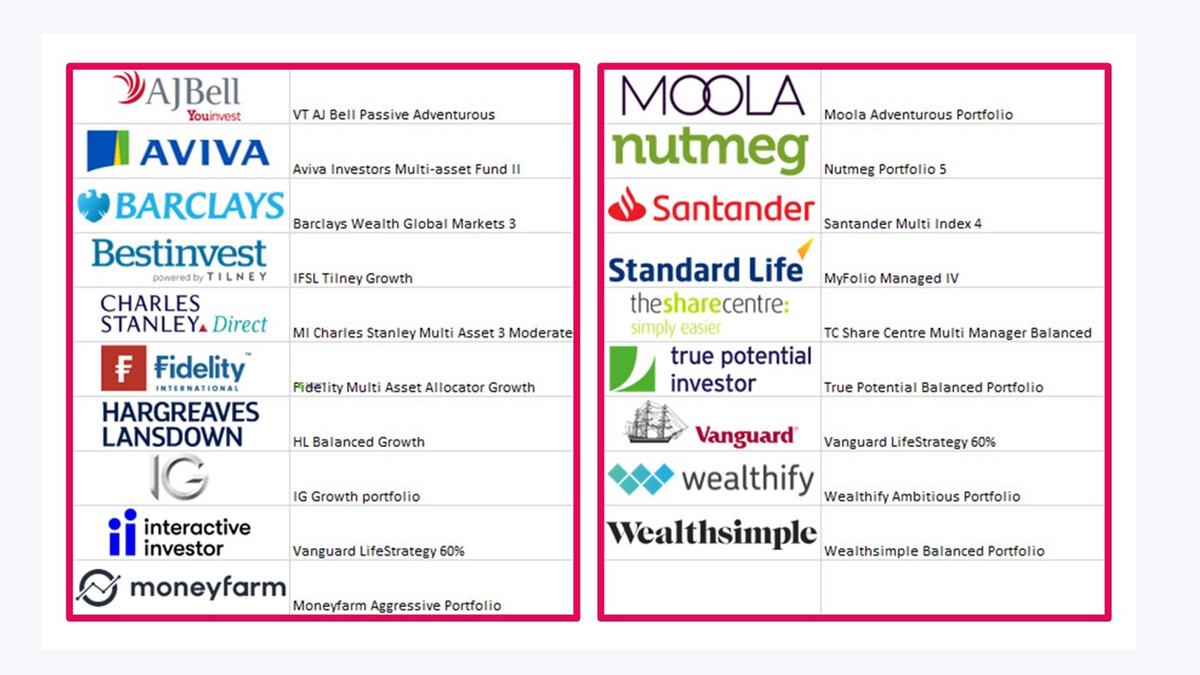

Which portfolios & funds do you hold?

Huge difference in ‘medium risk’ solutions – you might get a Korma or a Vindaloo

A DIY investor selecting a ‘medium risk’ option will be offered a wide range of different options.

Two years ago, our investment funds or portfolios had 60% in shares- or as close as was available. Just two years on and the picture has changed. The lesson here is to check in at least once a year and make sure that the thing you bought still looks like the thing you have!

And don’t assume they are all broadly the same. Hargreaves Lansdown’s portfolio had just 14% exposure to US markets compared to AJ Bell’s 41%. Aviva, Charles Stanley then Nutmeg had the lowest overall shares allocations with 40%, 44% and 46% respectively. The average % in shares of all 19 providers in the medium risk bracket was 53% as at January 2020 compared to a much higher 68% in January 2019. This tells us they collectively got spooked and moved en masse to safer pastures, holding less in shares, probably anticipating worse markets than we in fact saw.