Rookie Investor: Budgeting Apps

19 May, 2021

Welcome, Rookie

If you are a beginner when it comes to investing, and trying to find your way through this pretty complicated maze, you are not alone. Millions of newbies joined the ranks of DIY investors in 2020 as Tesla, tech stocks, crypto and clean energy captured our locked-down imaginations!

However, investing of course comes with risk. And trying to work out who to trust or where to start can fry the smartest brain. We’ve got some tips on how, where, and whether to start.

Should you be investing?

Although we believe that investing is typically the most sensible thing to do with long-term savings, it isn’t always right for everyone. We know markets can be bumpy so this isn’t a short-term game. And if you’re paying off expensive debt then it’s pointless investing on the one hand if you’re paying double-digit interest rates on the other.

Similarly, it's probably better not to invest if the risk seems too daunting right now and you’re likely to shriek and bail the first time that markets have a shocker. You do need to be able to stomach some ups and downs. It is also important to have at least a few months worth of cash savings before you start putting significant chunks of money into investments.

If you’re not quite at the stage to Press Go then check out what we think are some helpful budgeting apps below. Build that cash safety net first and get the foundations in order.

But if it’s time to join the ranks of DIY investors, we’ll help you find the best home for your stocks and shares ISA - typically the 'no-brainer' tax free account to start with.

Saving Apps - What are they and how do they work?

How is a saving app any better than totting up the difference between what you earn and what you save on the back of a post-it note, or even a more sophisticated excel document?

Saving apps seamlessly integrate with your bank account using clever AI and new open-banking technology, giving them the ability to analyse your incomings and outgoings, assess your salary, overdraft, debt, monthly subscriptions and more to calculate how much you can afford to put aside each month.

It then does what we often struggle to do and actually puts that money aside for us, into a separate pot or account, where it sits collecting interest, far enough away for us to think twice before spending it but close enough for us to access it if we really need it.

It's the nerdier, more sensible version of you!

The Apps – What are my options? Which one should I get?

There are more and more apps emerging in this space. Here we review three we like. You can read additional detail here.

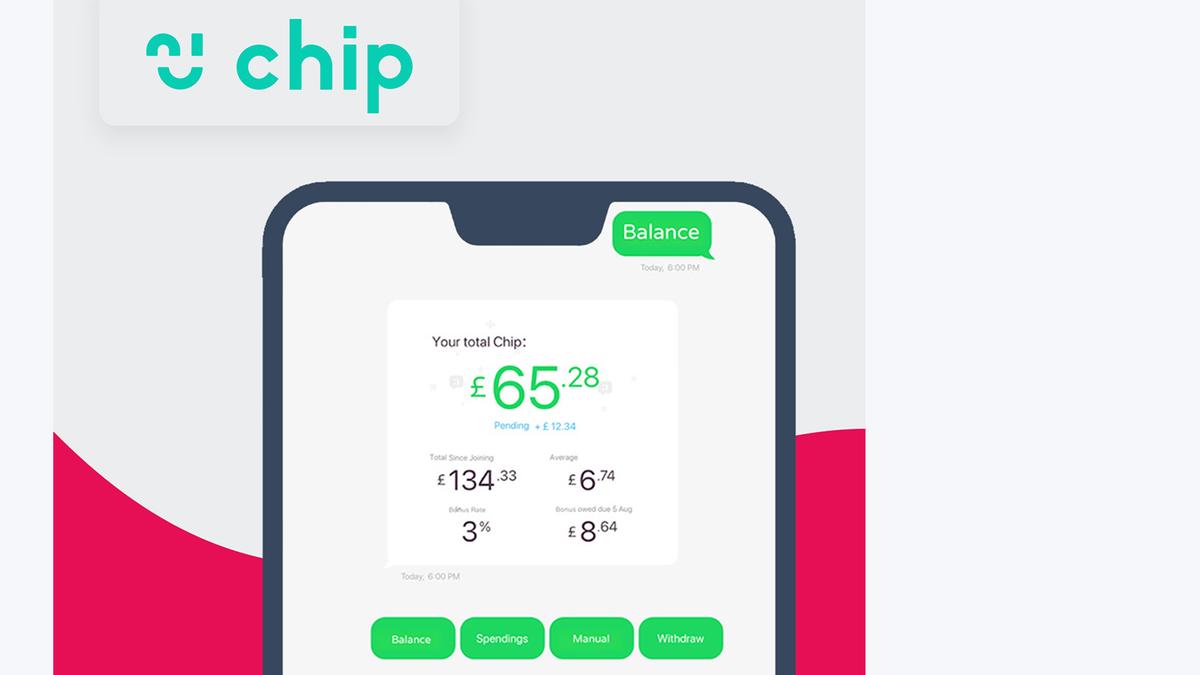

Chip

Best savings rate in the market

AI saving costs £1.50 per month

In the process of launching investment plan

ChipLite: Free / No autosaves and 1.25% interest on £2k worth of savings.

ChipAI: £1.50 per month / Auto saving features and 1.25% interest rate on up to £10k worth of savings.

ChipX: £3 per month / Investment plans and a Stocks & Shares ISA

Our View

Chip is a good option, its clean and easy to use. The free version has pretty limited functionality - it is very similar to what you get from Monzo, other than the amazing 1.25% interest rate on offer! This alone makes it worth downloading. The £1.50 per month AI plan is good value for money and brings Chip's USPs to light. For those that take advantage of the interest rate and the increased savings allowance that comes with the AI plan, the app more than pays for itself.

Overview

Chip is a savings app moving from strength to strength and currently offers market-leading 1.25% interest rate! There are host of different plan options and feature updates, with Chip in the process of launching investment plans in partnership with BlackRock.

ChipLite

Chip’s free ‘ChipLite’ plan connects to your bank and allows you to manually save money into instant/easy access savings accounts that pay a range of interest rates. The Chip+1 1.25% interest rate is only available to those who either refer a friend to Chip or are themselves referred to Chip and non-paying users can gain the interest rate on up to £2k worth of savings. Users can create pots for their different saving goals, which work effectivelyidentically to Monzo’s and other fintech banks.

ChipAI

The ChipAI plan is where things get more tantalising, with the 1.25% interest rate extended to cover up to £10k worth of savings. As the plan name suggests, users can then benefit from Chip’s AI features, which uses a fancy algorithm to autosave money and help boost your savings without you even realising.

ChipX

The ‘Chip X’ plan offers the added bonus of investment plans and a Stocks & Shares ISA, allowing users to invest their surplus money instead of leaving it in cash savings. This is priced at £3 per month and offers a convenient, affordable route for Chip users into the market.

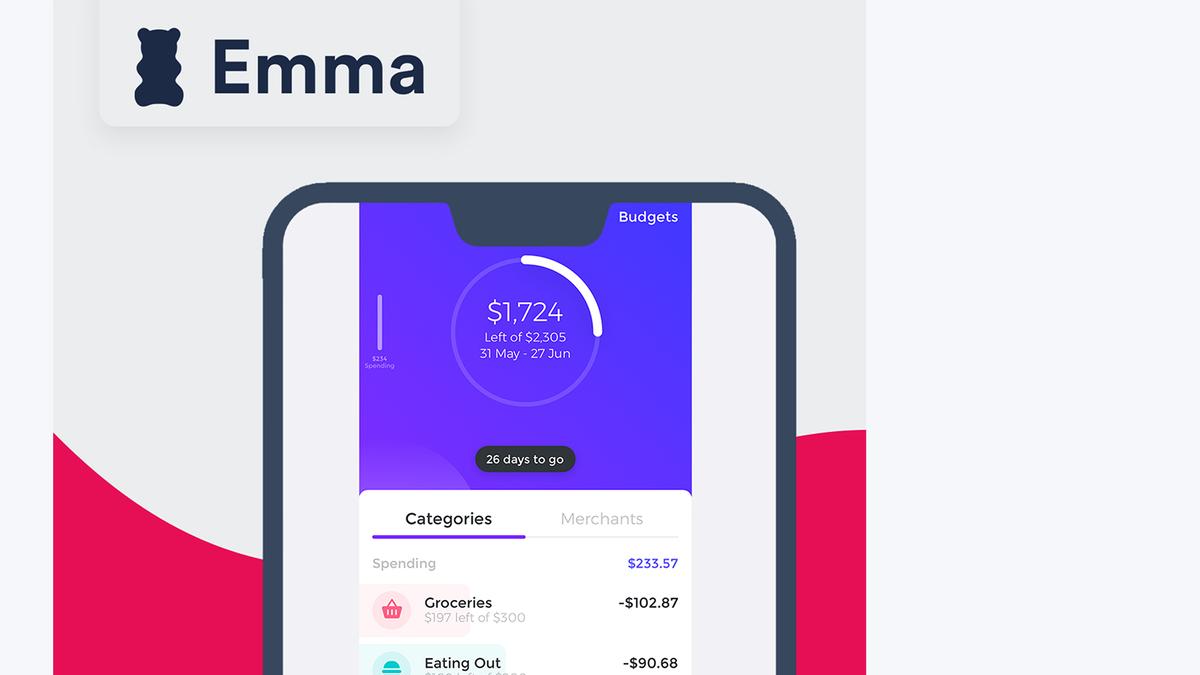

Emma

A holistic view of finances, inc investments, and credit cards

Good budgeting features

Many useful features available on the free version

Emma: Free

Emma Pro: £4.99 per month / Double cashback opportunities, the ability to manually add assets for more accurate net worth figures, exporting data, and a new rolling budgets feature.

Our View

Emma is more a budgeting app than a savings app, providing you with insights and analysis into your spending habits, and helping you allocate realistic monthly amounts to different spending categories. The linking of credit cards, bank accounts and investments really helps to provide an accurate overall picture of your finances. Having the free version is a no-brainer; but the £60 annual fee for Emma Pro feels steep, compounded by the fact that you can only pay it as a lump sum.

Overview

Emma’s key strengths lie in its spending analysis and overall ‘net worth’ presentation, with the app incorporating current accounts, savings, credit cards, and investments (inc Crypto!). Linking Emma to other apps is a smooth process, whilst having a holistic view of your finances, transactions, and incomings clearly displayed is a very useful feature. The budgeting capabilities of the app stand out when compared to other saving apps - this is an area where it can provide a lot of value.

Emma also recognises monthly subscriptions, showing upcoming committed expenditures separately, which gives you the chance to review them. For many users it may also highlight subscriptions to multiple similar services, such as Spotify and Apple Music, and suggest cancelling one to help you save some more money.

The app instantly analyses and categorises your spending, however, is very open to being customised and having its assumptions altered. This is a vital feature as users can exclude certain transactions from being included within Emma’s analysis, re-categorise expenditure and re-classify subscriptions, creating a more accurate and personalised outcome.

The user interface is intuitive and navigating through the app is straightforward. The design is slick and it definitely gives off strong new-age fintech vibes.

Emma Pro

Notable additional features on Emma Pro are double cashback opportunities, the ability to manually add assets or bank/investment accounts that the app doesn’t currently link to, as well as export data and benefit from a new rolling budgets feature. While these are definitely nice-to-haves, for most people they won’t justify the £60 Emma Pro annual fee (reduced to £30 if you subscribe within 24h of opening your account). Emma Pro is promoted quite aggressively on the app, which is slightly annoying albeit completely understandable considering how much you’re getting for free.

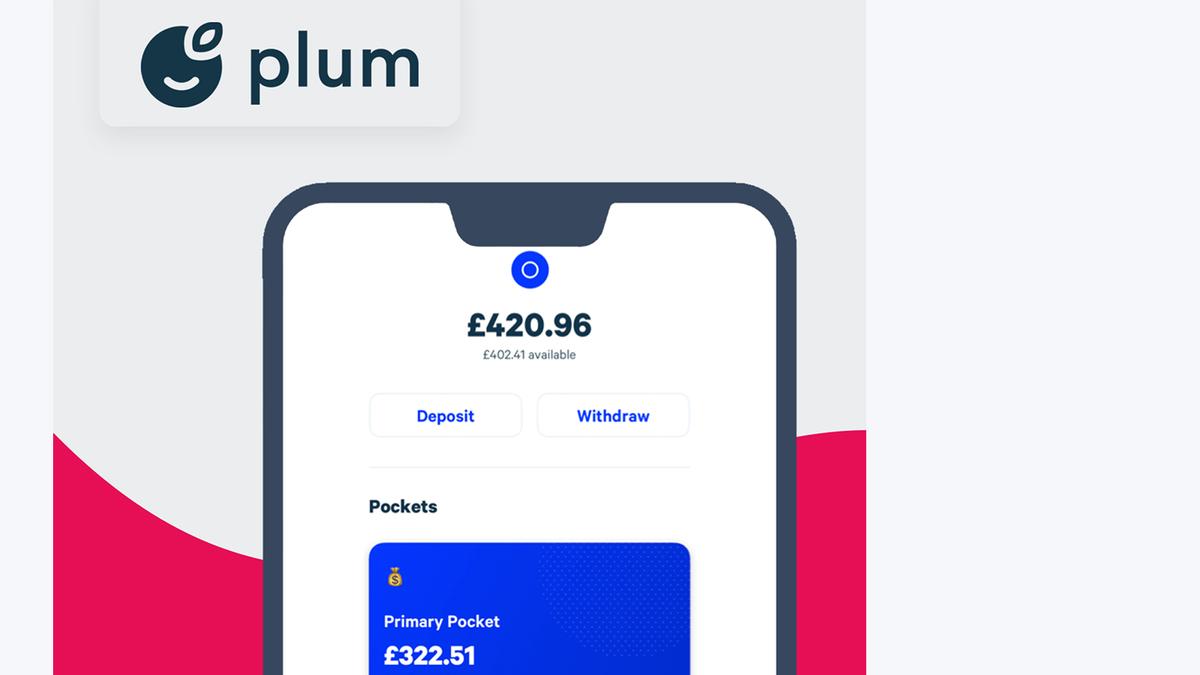

Plum

Strong algorithm and AI capabilities

Cool features that encourage extra savings

Option to invest as well as save

Plum: Free / AI auto saving is free.

Plum Plus: £1 per month / 0.4% interest, investments.

Plum Pro: £2.99 per month / Rainy Days and 52-week challenge, cashback, goals, diagnostic reports.

Plum Ultra: £4.99 per month / Money Maximiser.

Our View

Plum is an amazing savings app for those who need help putting money aside. The algorithm is impressive, effectively managing to squirrel away a lot more than you’d expect, without you even noticing! This comes with the added bonus of being absolutely free.

Overview

Plum is primarily a saving app that uses a “magic” algorithm to calculate the perfect amount of money to save, without the user feeling the money’s absence. Users can choose the aggressiveness of Plum’s algorithm from multiple options and have the freedom to change this at their own discretion. Plum takes the money from your bank account and puts it into a “pocket” on the app, which effectively operates as a savings pot that earns interest.

Plum Free

The free version of plum also comes with a round-up feature, which (as the name suggests) rounds up all your transactions to the nearest pound and collects this surplus money once a week, to deposit into your Plum pocket as extra savings.

Plum Plus

Plum Plus provides users with the option to invest for a £1 per month platform fee. Users have access to 12 different funds, which are named based on the individual fund’s overarching theme. The number of chilies next to the fund denote its risk level.

Popular Questions

Q: What if the app saves too much?

A: If at any point you want to withdraw money from your saving pot or overrule the AI, you can. You can also adjust the settings to tone down the aggressiveness of the AI's saving level in the future. This gives you complete power over the app whenever you want

Q: Can investing help me pay off my credit card debt?

A: Technically yes, but in reality, absolutely not. The best thing you can do to reduce the weight and drag of credit card debt is to channel all of your resources and spare money into paying it off as quickly as possible. It only makes sense to invest surplus money if you are anticipating performance growth greater than the interest rate you're currently paying. And in 99.99% of scenarios that will not happen.

Q: Why should I have 3 months savings before investing?

A: If you don't have savings for a rainy day and something happens that leaves you needing some extra cash, you don't want to be in a position where your only choice is to sell your investments. Especially if the market isn't doing particularly great and your investments have decreased in value.