What is a SIPP? What are the benefits?

12 Nov, 2021

A SIPP is an abbreviation for a Self-Invested Personal Pension, which is, as the name suggests, a pension that gives you the freedom to choose your own investments.

How are SIPPs helpful for investors?

SIPPs can be a key tool in saving up for a decent retirement and come with some important benefits, most interestingly, tax advantages. If you are a basic rate taxpayer, for example, the government will add in an extra 20% (so-called ‘tax relief’) on top of any contribution you make. So, if you invest £800 into your SIPP, the government will add an extra £200 to the pot, taking your account balance up to £1,000*.

This top up happens straight away, so your bigger pot will benefit from any stock market gains from the get go. For forward-thinking investors, especially those in their 20s, 30s and 40s, regular contributions and instant government top-ups, along with some sensible investments, has the potential to grow into a chunky retirement pot.

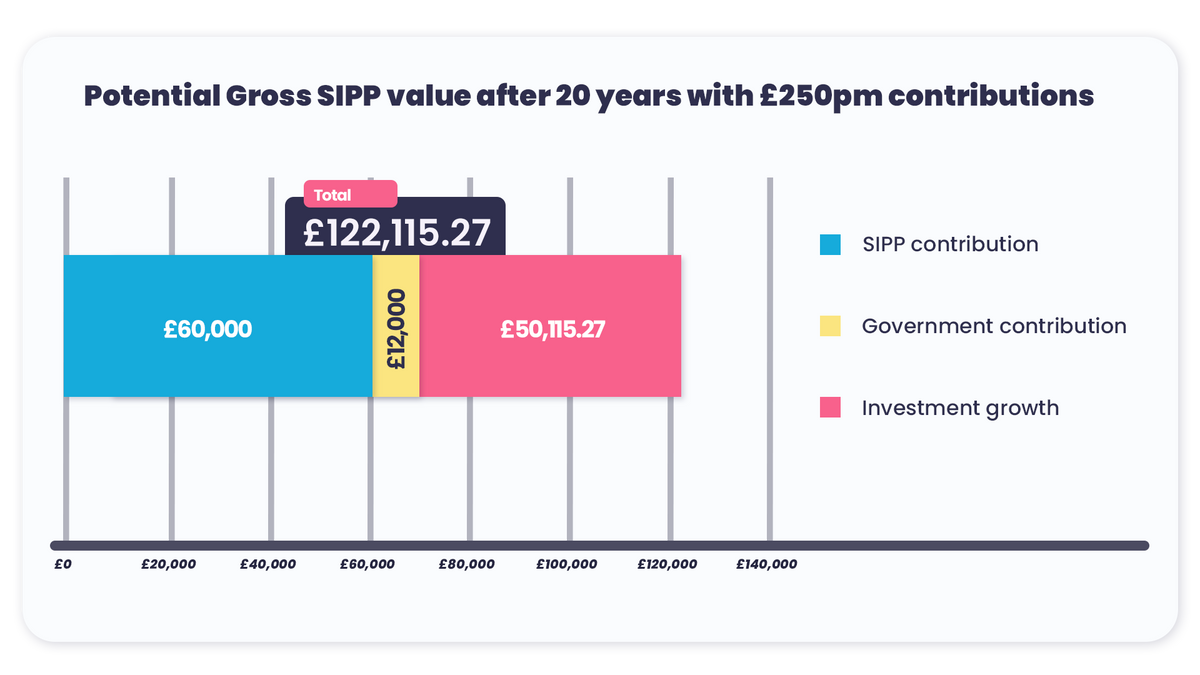

Let compounding work its magic

Albert Einstein reportedly described compound interest as the 8th wonder of the world and this is a particularly important lesson for younger investors with time up their sleeves. The graphic below models a £250 per month SIPP contribution, growing at 5% annually, across 20 years. The investment growth potential from consistent contributions is striking, with £60,000 of staggered contributions turning into over £120,000.

Why Freetrade?

Costs can impact the value of your portfolio significantly, especially with larger pots and longer timeframes, which are two fundamental characteristics of pensions. Investors can profit from substantial savings through Freetrade, through both low platform fees and non-existent trading fees. Platform fees are the cost you pay for using the platform and are essentially an admin fee charged for the service platforms are offering. Trading charges are the fee incurred for buying an investment.

Pricing models

There are two main pricing models for platform fees – one is a percentage fee and the other is a fixed fee. AJ Bell and Hargreaves Lansdown are two prominent advocates of the percentage model, charging an annual 0.25% and 0.45% respectively. Percentage fee models are cheaper for smaller portfolios, however, as your portfolio grows, their value for money decreases when compared to fixed-fee models.

Freetrade and Interactive Investor (ii) use a fixed fee model, which is more expensive for smaller portfolios but significantly cheaper for larger ones. Freetrade’s monthly SIPP fee is £9.99, or £7 if you have a Plus account with them already, leading to an annual platform charge of around £120; while ii charge £19.99 per month, coming in annually at around £240.

The table below shows the annual platform fee that users would pay on these 4 platforms, for varying portfolio sizes. Freetrade and ii’s fees don’t change, regardless of the amount invested.

With an average SIPP account worth about £100,000, Freetrade’s charges will save the average user about £100 a year compared to the mainstream competitors shown here. This can add up to several thousands of pounds across the lifetime of a pension.

Why should we save for retirement?

It is important to have a plan or some idea of how you’re expecting to fund your lifestyle after retirement. A few key elements of this include being aware of when you want to retire, what kind of lifestyle you’re expecting to have and how much money you should be investing in your SIPP now to make your future plans possible.

The last thing anyone wants after a lifetime of hard work is to approach retirement age and realise that either you have to work for another decade, or you need to make some major cuts to your quality of life. This is avoidable with foresight, planning and sensible investing.

A £40,000 annual salary leads to a monthly take home of approx £2,500. The table below shows you how much someone could accumulate over time, if they were to put 10% of this monthly take home pay (£250) into a Freetrade SIPP.

£250 per month | Contributions | Value | Growth (5% pa + Govt contributions) |

5 years | £15,000.00 | £19,807.45 | £4,807.45 |

10 years | £30,000.00 | £45,227.52 | £15,227.52 |

15 years | £45,000.00 | £77,850.58 | £32,850.58 |

20 years | £60,000.00 | £119,717.67 | £59,717.67 |

Compare this to a contribution of £400 per month…

£400 per month | Contributions | Value | Growth (5% pa + Govt contributions) |

5 years | £24,000.00 | £32,099.55 | £8,099.55 |

10 years | £48,000.00 | £73,294.79 | £25,294.79 |

15 years | £72,000.00 | £126,163.05 | £54,163.05 |

20 years | £96,000.00 | £194,012.00 | £98,012.00 |

As this clearly illustrates, consistent contributions across your working life can be the key to a comfortable retirement and the sooner you start, the more compound interest gives you a bang for your buck!

* These are pensions so read the small print! There is a limit to the Government’s generosity and so there are caps on how much you can pay into your pension every year and still receive tax relief. These won’t be a problem for most people – only the very affluent.

If you'd like to open or transfer a pension with Freetrade or learn more about their products click here.

This is sponsored content and was written in conjunction with Freetrade. As such, this content does not necessarily reflect the opinions of Boring Money. The cost calculations in this article were conducted by Boring Money’s independent research team. Reliance upon information in this material is at the sole discretion of the reader.