Annoyed Self-Employed

By Mike Narouei, Content Producer at Boring Money

24 June, 2021

The Basics

Ah yes, this is the life. As one of the growing ranks of Britain’s 5 million self-employed, you get to call the shots. You can pick and choose who you work for. You can spend the occasional day in a tracksuit. And you only have one bastard boss to worry about – and that’s you!

But to paraphrase Spider-Man, with great freedom comes great responsibility. Often buried beneath a mountain of paperwork, feeling like an unpaid VAT collector for HMRC, or wondering when those bigger clients are actually going to get around to paying you, you probably miss the days of having an IT helpdesk and a Chief Financial Officer. But that’s where we come in.

While we can’t do your paperwork for you or fix your tax returns, we’ve tackled three major topics that self-employed people tell us they struggle with. So buckle up, boss, and get ready for some straight-talking independent advice.

3 Things the bureaucrats can make harder

1. Business Banking

Although it can cost extra, it’s a legal requirement to have a business bank account if you’ve set yourself up as a limited company. If you’ve opted instead to be classed as a sole trader you can technically use your personal account, but it’s best not to. Keeping things separate makes it easier to complete your tax return and keeps the bank happy – they may threaten to close your personal account if you use it to peddle your wares.

2. Mortgages

Computer says no! As a self-employed person, prepare for a headache when applying for a mortgage. Although there aren’t separate products for the self-employed, the assessment stage is like a Cold War interrogation. But don’t worry, help is at hand on the following pages.

3. Pensions and Plans for Retirement

Think pensions are the least of your worries? Think again! With only 31% of self-employed people paying into a pension, the UK is going to have a real problem when we all start reaching retirement age. Unless you have some other savings to fall back on, you’ll have to keep on working until the bitter end. Get it sorted now – with low payments that might surprise you.

Which flavour of self-employed are you?

There are about 5 million self-employed people in the UK today, and you come in a colourful range of shapes and sizes. Some get a sweeter deal than others when it comes to rights and benefits, so it pays to know what you’re entitled to.

1. Self-employed or freelance

You probably know what rights you don’t get – pretty much everything. But you still have protection for health and safety and protection against discrimination. To make up for the rest, make sure you have backup plans like three months’ savings in cash and consider income protection insurance or critical illness cover.

2. Contractor

It’s a lottery for you, but you can improve your odds if you’re good at negotiating. Health and safety and discrimination will always be covered, but the rights you get depend on the contract you agree. As a rule of thumb, if you’re working with a client for over 3 months you should push to be classed as a ‘worker’ rather than a ‘contractor’ – they get more of the good stuff.

3. Gig worker

Recent court cases have ruled that some gig workers are ‘self-employed’ whereas others are classed as ‘workers’, which is a status that comes with basic holiday, National Minimum Wage and other benefits. Nobody really knows where to draw the line yet – helpful! – so keep an eye on the news and the Independent Workers Union website.

There are plenty more categories and sub-categories in this complex web of employment and tax statuses, so check out the Money Advice Service guides for more of the boring detail.

Should you set up shop as a limited company or sole trader?

Working out whether to remain a sole trader or whether to set up a limited company is often a question of tax.

A sole trader has less faff and paperwork but could pay more tax once annual income starts heading upwards of £50k. A limited company does mean you can take money out as lower taxed dividends, rather than as income, but the rules can be complex and depend on your situation.

It’s worth taking advice from an accountant. But for a quick outline, take a look at this article and try out this calculator.

Business Banking

Whether you think of yourself as a driver, carpenter or even a self-employed pilot, you’re the finance person too now. And that means setting up a bank account for your business. Yippee!

Business bank accounts operate differently to a normal bank account, with all sorts of add-on services from tax advice to funding, but also with extra charges. To make sure you don’t end up shelling out too much, you should first figure out what you actually need and what’s just extra fluff. Only then should you pick an account – they’re bloody hard to get rid of after the fact, as we found out not too long ago...

Just the same as personal banking? Hell no!

1. Understand the charges

You know exactly what goes into your beer batter/cement mix/SEO strategy, so why wouldn’t you take just as much care with other business-critical expenses? Instead of just comparing headline stats of each bank account, make sure you read the full T&Cs and fee structures. Boring, we know. But with your business on the line, it’s essential.

Will you be paying a fixed fee for every cheque and e-payment you receive?

Do ATM withdrawals or bank transfers come with a charge?

If you need an overdraft, are there daily or yearly costs for using it or going over the limit?

Think about how your business operates and what the implication of higher or lower fees will be. Some you can afford – others you can’t.

It’s not uncommon to find special deals where you don’t have to pay any fees at all for up to 24 months. Music to your ears? Absolutely. But it could be a siren song, leading you towards a hard fee structure that doesn’t suit your business model. Before you take any special deals, make sure the account still makes sense when it’s full price. High transaction fees, for example, could spell disaster for a cake shop that sells lots of low-value items, but would make little difference to a plumber.

2. Lending can be mind-bending

As with personal loans, you need to understand how the repayments and interest rates work. One bank may at first glance look better than another because it doesn’t charge an arrangement fee, but it makes up for it with a higher interest rate that could end up costing you more over time.

As lenders vary their rates according to how risky they think your business is, it can be tricky to compare like for like on a comparison website. One way to tell the goodies from the baddies is to look at industry awards like the Moneyfacts Awards.

For more tips around funding for your business – as well as for payroll and auto-enrolment – check out our Everyday Entrepreneur learning path.

3. Bells, whistles, and chocolate teapots

Try not to be dazzled by the included extras some banks use to tempt you. If you’re a travelling barber, you probably don’t need an import/export advice service, so why pay for an account with it included?

Having a resource like an in-branch business management team can be useful – it’s handy to get a sense check every now and then when you spend most of your time working alone – but make sure you aren’t paying for all the shiny extras in higher account charges. Sometimes it’s better to just find the service elsewhere and pay for it when you need it.

Which bank should you go for?

There’s no easy answer for this one – it depends on the services you’ll need. Your best bet is to use a comparison site that shows you more than just prices, and also to check what existing customers are saying. They know best.

We like the clarity of this table from MoneySuperMarket.

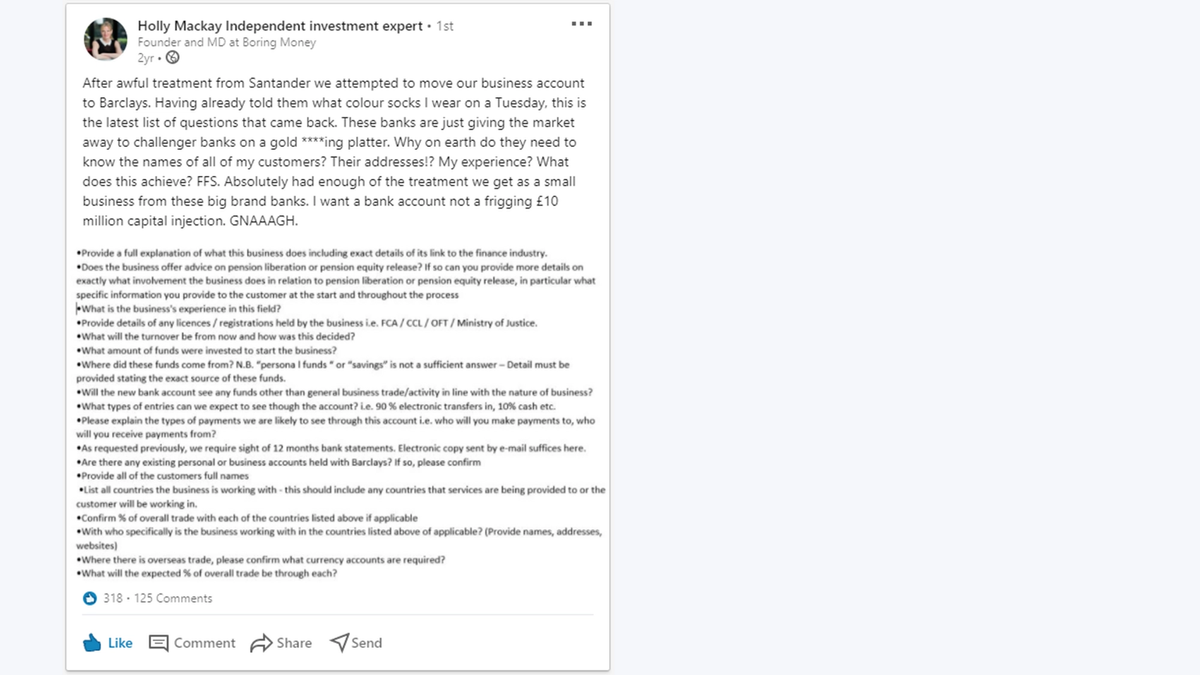

The great LinkedIn banking debacle

- I have been trying for over 6 months now to remove our old accountant from the contact records. And ex-staff members from company credit cards. I've written, I've emailed and I've called…

We were in the market for a new business bank account recently, and what with all the laundering checks and mumbo-jumbo, it’s clear that switching accounts today is not as easy as it used to be.

Frustrated with Santander and Barclays, we asked the people of LinkedIn for their recommendations. Based on this, it appears that Starling Bank and Metro get the thumbs-up.

Mortgages

Buying a flat? Got your eye on that vacant shop? Sounds like a job for a mortgage. But as you might have guessed, you’ll have a much harder time getting one if you’re self-employed. Annoyed isn’t the half of it.

Some lenders will flat-out refuse you before they even take a peek at your finances. To them, you’re too risky to bother with, seeing as about half of small businesses go kaput in their first 5 years. Fortunately there are plenty of other lenders who will give you the time of day, but getting through the dreaded assessment process is still an uphill struggle. Employed people don’t know how good they’ve got it.

What happened to self-certification?

It didn’t always feel like pulling teeth when applying for a mortgage. If you’ve been in the game for over a decade, you might remember self-certification mortgages, which were designed for people who find it harder to prove their income. People like the self-employed.

Unfortunately, the product was pulled after the financial crash of 2008. Lenders have since tightened up the rules and it can be tougher than ever to pass the income and affordability tests.

1. What to look for when choosing a mortgage

As a self-employed person, if you were to plot your monthly income on a chart, chances are it would probably look like a bird’s-eye-view of the Thames: up, down, all over the place. Irregular income makes it harder to plan for regular outgoings, such as mortgage repayments, so the main things you want to consider are flexibility and affordability.

If i have a slow month without much work, do I still have to make my full mortgage payment?

If my business tends to do better in summer, can I make most of my payments then and take a payment holiday in winter?

If my circumstances change, can I switch to a different loan without moving heaven and Earth?

These are key questions to ask when narrowing down your list of mortgage providers. Of course, the mortgage product you choose, the amount you borrow, and whether it’s affordable, depends on your own unique needs – there’s no difference between ‘normal’ mortgage products and those for the self-employed. It’s only in the assessment stage that you’ll start to feel the strain…

2. Running the assessment gauntlet

Even Olympic athletes and household-name heavy metal stars have a hard time getting approved for a mortgage, according to Andy Deeley of Family Building Society. The biggest hurdle is being able to prove your income without a bog-standard wage slip at the end of every month. Another common difficulty is, sadly, being old. The fewer working years you have left in you (in the lender’s eyes), the lower your chances of being approved. So how can you load the dice back in your favour?

Big vs Small: size matters in mortgage providers

Does bigger mean better for me? If your business has a solid track record, a library full of account paperwork, and enough income to show up on the big lenders’ radars, go for the big lenders (or at least try them first). Banks like HSBC and Nationwide can afford to give you lower interest rates than smaller independent lenders, but they can also afford to cherry-pick the market for the least risky borrowers. That means being accepted is much harder. If the computer says no, that’s your lot.

Will good things come in small packages? Most self-employed people will be better off with a smaller lender, because they’re able to take a holistic view of your accounts and look at individual cases. That means you’re more likely to be accepted, but you’ll probably have to pay a higher rate of interest. If it’s the difference between getting a mortgage and not getting a mortgage, that seems like a fair trade-off to us.

To compare a range of mortgages that could be suitable for self-employed people like you, take a look at this list to get started.

Pensions and long term plans

Red alert! You may have heard about the so-called self-employed pensions crisis, concerned with generations of Brits reaching retirement age with nothing, nada, zip to live on. Unlike employees, who get auto-enrolled onto a workplace pension, the self-employed have to take the initiative and find their own private pension – and only 31% of you are. So instead of playing with your grandkids or escaping to a Spanish villa, people like you might have to hustle, commute and slave away till you pop your clogs. And that’s putting it nicely.

With no boss to sort this out for you, the ball really is in your court. Thankfully, unlike mortgages, there are no barriers to you starting a private pension online. And you can do so with a direct debit of as little as £25 a month. Plus, here is the biggest perk of a pension – free money!

For every £80 you save into a pension

The government adds an extra £20

(Plus you can claim another £20 if you’re a higher tax bracket earner.)

More about tax relief.

1. What's been stopping you from sorting out your pension?

I’m too busy with the day-to-day…

But it only takes 10 minutes to set up a DIY pension online.

My irregular income makes saving difficult…

But you don’t have to commit to regular payments – just pay in what you can, when you can, from about £50 a month. The sooner you start, the more time you have to earn interest on it.

There’s already a state pension…

Yeah, and it currently pays out a whopping £175.20 a week. That sounds like a fun retirement.

I need my money now, not later…

You won’t be saying that when you’re working into your 70s and 80s. A little saving now makes a big difference later.

My business is my pension…

Ok, fair enough. If your business is realistically something you can sell for enough money to support you for (hopefully) 2 to 3 decades, that works too. But all your eggs are in one basket.

I don’t know what good looks like…

You’re not alone – this is one the biggest barriers for the self-employed. But as long as you start saving somewhere and earning the free government money, and as long as the profit you earn from that money being invested outweighs what you pay in fees (pensions are invested in the stock market, by the way), then you’ll be okay. You can always switch pension if you find a better deal.

2. Understand the nitty-gritty in 10 seconds

You get free money from the government on the first £40,000 you save every year. At least an extra £20 on every £80 you save.

You can pay in up to £1,073,100 tax-free over your lifetime.

Your savings are invested in the stock market to help them grow. You can do this yourself with a SIPP (self-invested personal pension) or have a professional choose for you.

Your money is locked away until you're 55+ (57 from 2028)

For everything else, like working out how much you’ll need to save, head over to our Private Pensions investing guide.

3. Get started online in only 10 minutes

From as little as £50 a month (with payment holidays if you need them) you can start working towards a more secure future. Use our Best Buys table to find a list of suitable providers, then shop around to find a deal that suits your circumstances. Online applications should only take about 10 minutes.

Shop around for a provider that:

Has a history of high performance, getting good returns on investments (though remember that past performance can’t guarantee continued good luck).

Doesn’t cost an arm and a leg. Fees up to 1% of your pension pot a year tend to be reasonable, but if you’re looking at 3% then ask why it’s justified.

Allows for flexible contributions. As someone who’s self-employed, your monthly earnings likely go up and down, so make sure you can miss payments without facing a penalty and can pay in lump sums when you have a good month.

4. What do customers recommend?

Check out our Best Buys table and filter by product type to read our own independent ratings and customer reviews of UK pension providers.

Hargreaves Lansdown score well on service – reassuringly pricey and the Waitrose of pensions. AJ Bell Youinvest are more like Sainsburys – decent, solid and everyday. And Aviva is probably the Morrisons – a large brand, low on frills, which offers a decent and simple service for people who want a household name.

5. What are you other retirement options?

Business as pension: Some people intend to sell their business and live off the lump sum – a risky move unless you’re completely confident you can pull it off.

Lifetime ISA: If you’re 18 to 40 years old you qualify to open a LISA, a savings account with a 25% government top-up. Use this calculator to see if you’d be better off with a LISA.

Go off-grid: If you’re handy with an axe and know which berries are edible you could join the 75,000 Brits living off the land. Though saving for a pension is easier.

Try the Retirement Income Options tool

Set aside half an hour or so to really consider your options, using this fantastic, detailed

Retirement Income Options tool from Money Advice Service.

Your Options

1. Financial advisors - should you pay for one?

They used to have a bad name, surrounded by tales of greased palms and bias towards certain pension providers, but not anymore. Since 2012, new regulations mean IFAs (independent financial advisors) no longer get built-in commissions, but you have to pay for their advice. And generally speaking, it’s worth it.

They can search the whole market and make a recommendation that’s tailored to you.

They can help you make a realistic plan that considers lifestyle and family as well as taxes and interest rates.

Plus, you’re protected if the product you buy turns out to be unsuitable or in the unlikely event the provider goes bust.

Sir Steve Webb, former Pensions Minister, told us:

- In our research, we found that people who take financial advice are on average £40,000 better off over 10 years. The principle reason is that they take appropriate levels of risk in the long-term and make good returns on their investments.

Read more of the Steve Webb interview

Search for and compare financial advisors

Ask: How to choose a financial advisor

2. Banking, mortgages and pensions - which are best?

Remember, these are the cornerstones of your empire. As always, we don’t think you can find a more accurate review of a service than one by an existing customer. So check out our Best Buys for genuine testimonials as well as our expert analysis and opinion.

Compare our Best Buys for pensions (https://www.boringmoney.co.uk/isas-pensions/) (tick the ‘pensions’ filter box)

Compare mortgage providers (remember that flexibility is key)

Taking a loan? Find out what your credit score has to do with it. And use this loan repayment calculator to work out if it’s affordable

3. All the other guff - does it ever end?

Taxes

How to complete your Self Assessment tax return =

Expenses

Insurance

Business insurance for your equipment, goods and liabilities

Business indemnity insurance for customers making claims against you

Getting paid

Work out what to charge with this freelance rate calculator

Your options for chasing late payments

Extra help and support

Money Advice Service guides for the self-employed

Gov.uk webinars and courses for the self-employed

You may also like...