Retirement

By Mike Narouei, Content Producer at Boring Money

22 June, 2021

The Basics

1. What Are The Timeframes?

The current rules say that you can dip into your pension savings from the age of 55 but – spoiler alert – it’s going up and will rise to 57 in 2028.

The state pension age is increasing and it’s set to reach 67 for both men and women by 2028.

Importantly though don't take these ages as gospel when planning your retirement- no-one can tell you when you have to retire!

2. What Will Make Up My Retirement Income?

There are three basic chunks.

a) The State Pension,

b) any pension from your work and

c) any private pensions.

Of course you can also top up your income with any ISAs you have, interest on cash and any income from properties you might rent out.

3. The State Pension

The full state pension is around £9,110 a year. BUT you have to have been working and paying National Insurance for a full 35 years to get this. If you want an indicator of how much your weekly State Pension will be then go to HMRC for a projection. This is the first chunk of the total.

If this is horribly low then you have 3 choices. Retire later. Or save more privately. Or pay top-ups to your National Insurance which get you a chunkier State Pension when you retire.

This isn't as complicated as it sounds and you can check your National Insurance record here. You'll need your Government Gateway details/have to set this up.

4. Workplace Pension

The law changed in 2017 (ish) and everyone over 22 who earns more than about £10,000 a year has to be offered a pension at work by law. The numbers are crunched as follows – take your salary between about £5,000 and £45,000. This sum is your ‘qualifying earnings’.

5% of this amount goes into your pension instead of into your pay packet. And about 3% extra comes from your employer. Do try not to opt-out if you can possibly avoid it. That’s like saying to your boss “No thank you, you can take that free extra 3% pay rise and stick it.”

Let's give an example. If you earn £50,000 a year then this works out as monthly contributions of about £270 or £3,240 a year.

If you're 40 and plan on retiring at 65, then £270 a month assuming stock market returns of 5% a year would tot up to about £160,000 in your pension stash.

*All sorts of assumptions there which might go wrong for numerous reasons - back of a fag packet only folks.

5. Private Pension

It really is easier than ever to set up a private pension. If you do, you will get free money from the Government. Honestly!

Poorly understood 'tax relief' basically means that the Government will give basic rate tax payers a free £20 for every £80 they save into a pension. And if you're a higher rate taxpayer you can claim an additional £20 back when you do your tax return.

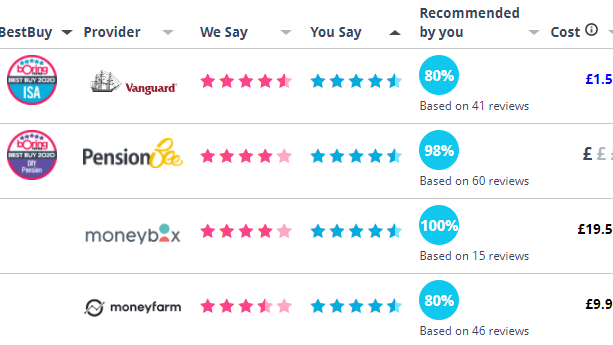

Feeling apathetic? You can start one online in 10 minutes with a direct debit from as little as £25 a month – more often than not it’s £50 a month. So even if you are “not the sort of person who does this” – maybe read on? Don’t get mad, get even? Our Best Buys will show you who we rate. And who our readers rate.

6. How Do I Actually Do it!?!

Behind all the jargon, a pension is just like a 'financial drawer' in your personal money chest of drawers! You stick in some money and this money is kept separate from your other money, in a specific pension account. This is because there are different rules about when you can get it and how much tax you pay on it.

These days the interesting bit is that you can decide what to put into your pension drawer. You don't just send your money off into some faceless company to be managed by a nameless production line. You can open up a DIY pension online, pay in a monthly direct debit, and choose shares, funds or other investments. And if you haven't really got a clue and just want to invest in a broad mix which is sensible, then there are groups which will do all of the selection and management for you. Our Best Buys pages let you filter pensions options by your levels of investment knowledge so don't be put off.

Free Money

1. Tax Relief Is Sexier Than It Sounds

Put into normal speak here's the deal. The Government is mildly alarmed that it will have an army of oldies living for ages and sucking the money out of their coffers. So they want to persuade us to save for our retirement so that they dont have a monumental care crisis.

So they give us an incentive. If you're a basic rate taxpayer, for every £80 you pay into a pension, the Government will add another £20.

FREE!

The news gets better if you're a higher rate taxpayer because as well as the £20 for every £80, you can also claim back another £20 on your tax return. So saving £100 into a pension effectively costs you £60.

Hargreaves Lansdown has a pension tax relief calculator here.

2. There Are Limits To The Feebies

The Government's largesse is not unlimited.

The basic rule is that pensions contributions are limited to £40,000 a year. And you cannot contribute more than your income.

This might all sound like wishful thinking but if you've inherited some money, had a redundancy or some other lump sum then just be aware that there are limits to annual contributions.

If you have not paid any money into a pension for the previous three years, then you can add up these allowances ie pay in more.

The independent Pensions Advisory Service has more details here.

Pension MOT

1. Do You Know What You've Got?

This means turning out that drawer, leafing through ancient correspondence and working out where you have pensions. Go back through every place you’ve ever worked and try and remember if you had a pension as part of your employee benefits. Pension schemes of which you’ve been a member should be sending you a statement each year but they may well not know how to find you.

Tip: If you’ve moved and they’ve lost you, don’t panic. There is a dedicated government service to help you track down ancient pensions. You can also approach the pension provider or your old employer if you’re no longer getting statements. It’s worth drafting up a generic letter and sending it to old employers – when did you work at the company and how can you trace your pension?

The bald-faced truth is that there isn't a pain-free way to do this. Just think of the money.

2. How Strong Is Your Cocktail?

We think of your total income in retirement as three different ‘shots’ which get mixed together to make the total. This short Guide will help you to work out a rough estimate of how much you will be able to chuck into each glass – and how strong your cocktail will be. Hic

The First Shot: State Pensions

These are funded from National Insurance (NI) contributions and are intended to ensure we all have a basic amount of money to support us in our old age. The new State Pension is currently £175.20 a week BUT you’ll get nada if you haven’t got at least 10 years of NI contributions under your belt from working (or the relevant ‘credits’ from periods of illness of unemployment.)

The Second Shot: Workplace Pensions

From this year you have to put in at least 5% of your salary (or ‘qualifying earnings’ which for the 2020/21 tax year is between £6,240 and £50,000 a year). The Government will bung in an extra 1% and your employer has to put in at least 3%. So that’s 8% which will be building up, month after month. The more you earn, the more you will save. You can refuse to take part (“opt out”), but it’s not a great idea because you’ll forfeit the 3% from your employer and 1% from the government.

The Third Shot: Private Pensions

These are pensions which you set up by yourself – a bit like you would an ISA, or buying insurance online yourself. You choose the pension and you choose how much you can afford to put away each month. If you’re about 40 and save £25 a month, you could save a stash of about £21,000 by your retirement age. Assuming you take no tax-free cash, this would give you a pension of about £24 a week. This might all sound horribly boring BUT, if you’re a basic rate tax payer, for every £80 you put in, the Government will top it up with another £20. That’s free money. Higher rate tax payers can claim back even more – another £20 come tax return time. Interested? See who we rate on our Compare pages.

3. Bringing It All Under One Roof

Consolidation can be a good option if you’ve built up a number of pension pots during your working life. You may also get cheaper % fees from pension providers with a larger pot. Combining them is a bit of an administrative hassle, but it’s not super-difficult.

Be warned, your pension provider may charge you, so before you instruct any moves do phone them (boring, sorry) and ask them to walk you through any applicable exit fees. Some larger schemes are now so low cost than frankly it’s better to let sleeping dogs lie.

Also if you have an old defined benefit or final salary scheme be very careful about moving this. Anything with the word ‘guarantees’ in the paperwork is probably quite valuable and not worth cashing in without understanding fully what you’re doing.

You may want to consider getting financial advice. This doesn't need to be a horrible process these days! Costs of advice have been split from any product sales so the murky world of commission has gone. Spend between £150 to £250 an hour or pay an ongoing fee of about 0.5% - 1% a year. If these guys save you from unnecessary tax or sitting in the wrong investments, they will pay for themselves....

Tip: You can now consolidate your pensions into one account managed online. These guys want your business and so get them to do all the nasty consolidation paperwork for you. You can send them a note with all your existing pensions and tell them to transfer them over. Have a look at our Best Buys pages for what we think about pensions providers – and what other customers think.

Things To Watch

1. Annual Allowance

Covered in the free money section - mind you don't break the basic £40,000 a year rule.

2. Lifetime Allowance

You do need to watch that you don't amass more than the current Lifetime Allowance of £1,073,100 in your pension pot or you will get smacked with tax. (Don't spit out your cornflakes - this is actually easier done than you might think if you start saving pretty early or have a decent middle management role with a generous pension.) Read up on the Lifetime Allowance if you need to.

3. Tax

The basic deal is that you can take 25% of your pension out and not pay tax. The rest is taxed as income.

Now here's where you can be clever. You don't want to get to 55, shout HOORAY IT'S ALL MINE and then take out so much for a post-midlife-crisis-new-car that it pushes you into being a higher-rate taxpayer that year if you can avoid it. This pension is income and treated as such by HMRC.

The other thing to watch is tax codes. Talk to your pension provider - you want to avoid getting an 'emergency tax code' on any lump sum you take out. This works on a 'Month 1' basis and assumes you'll be taking that amount out every month so you only get 1/12th of your personal allowance applied instead of the whole lot. Resulting in a whopping tax bill. One trick is to take out a small amount initially say £100, let the tax code adjust and then take out what you need. This can be head-bangingly complicated so talk to your platform or pension provider.

4. Financial Advice

We think there are many times when we can self-serve. Saving into an ISA for example. We don't really need financial advice for that. But pensions are complicated and a bad call can cost you thousands. Even if you are deeply sceptical about financial advice or have been burnt in the past, these days advisers are better qualified than ever and charge fees not commission. Why not consider trying to find someone who will give you 5 or 6 hours of advice to guide you through the at retirement process and help you avoid any clangers?

Expect to pay between about £120 and £250 an hour depending on where you live and who you see. CFP are the letters which mean the highest levels of qualifications although experience and good feedback are also pretty important. Look at our directory to see advisers in your area.

Your Options

1. When Saving Up

This doesn't have to be complicated. Just start. It's much more important to start early than it is to get the most swottily perfect investment portfolio.

If you don't know where to start look at our Best Buys. Filter by options for beginners. If you're savvy then fill your boots with the platforms. Or just stick £25 a month into a very vanilla bog standard FTSE 100 'tracker' from someone big like iShares. Procrastination is the enemy here as lovely juicy compound interest is a young person's friend when it comes to pensions.

Finally if you have lots of little pensions scattered around from previous roles, have a think about PensionBee which is a nice new digital service which will consolidate all your old pensions into one new shiny digitally accessible savings pot.

2. Annuity Or Drawdown

You have 2 main choices.

Annuities are the old-fashioned option. You engage with a pension company and say "OK. I have £200,000 in my pensions today. If I give that all to you today, what will you promise to pay me an an annual basis until the day I die?"

Effectively the actuaries behind the scenes are trying to work out when you might die. Charming.

The benefits are that you get certainty. The money won't run out. But rates are a bit rubbish as it's all pegged to interest rates which are low these days.

Try this calculator from the Government funded and impartial Money Advice Service.

Drawdown has soared in popularity with more flexible rules around pensions. This is keeping some 'skin in the game'. "I'm going to take my pension stash, have my 25% tax free cash off the top, then put the rest in the stock market, hope it grows, and take income out when I need it. And hope it doesn't run out. "

If invested well, you will probably get more from this route than from an annuity. But no-one gives you a fixed sum every year that can be relied on.

We think drawdown is probably the better route but get some advice on at least the set up if you need to. You're better off trying to find an adviser to give £1,000 to for this project, rather than tackling it alone if unsure.

3. When Drawing Down

There are 2 big decisions. Do you want a regular income or do you just want this thing to grow as much as possible within reasonable risk parameters. If you're after income then have a look at Equity Income funds. (We have some ideas in our Funds section or look at the best buy lists on groups like Hargreaves Lansdown or Charles Stanley.) If it's growth then look at Growth funds.

Not sure? Our big tip here is to consider getting some financial advice to make sure you're not doing something expensive and wrong. Even just buying a few hours with someone. You need to do some basic cashflow modelling and work out how much you can drawdown without leaving yourself high and dry in later life.

The Government also has a free service called The Pensions Advisory Service which is staffed by hugely knowledgeable people and has the benefit of being free. Try calling them.

And finally if you have a defined benefit pension, or a final salary scheme, be really wary about moving it or fiddling with it. They can be very valuable and it's easy to underestimate the long-term benefits so do be wary about moves or changes.

4. What To Pay

When saving into a pension, you should expect to pay about 1% all-in. This should cover administration charges and also investment charges. If it's more than 1.3% all-in every year then that's too high. (This doesn't include advice fees which will be extra and which will be justified and deserved if your adviser is doing a good job.)

Drawdown is a little more complicated. Expect to pay about 0.25% - 0.75% for investment funds. And about 0.25% - 0.5% for administration. And then there is often a menu of charges to kickstart drawdown, and an annual £ fee to receive regular payments. It's quite complex and tricky to compare - sorry - don't shoot the messenger.

Compare charges using our Compare pages here.