How do stocks, bonds and cash perform when the Fed starts cutting rates?

New long-term analysis digging into returns during 22 cutting cycles since 1928

13 Feb, 2024

By Duncan Lamont, Head of Strategic Research Unit at Schroders

Sponsored by Schroders

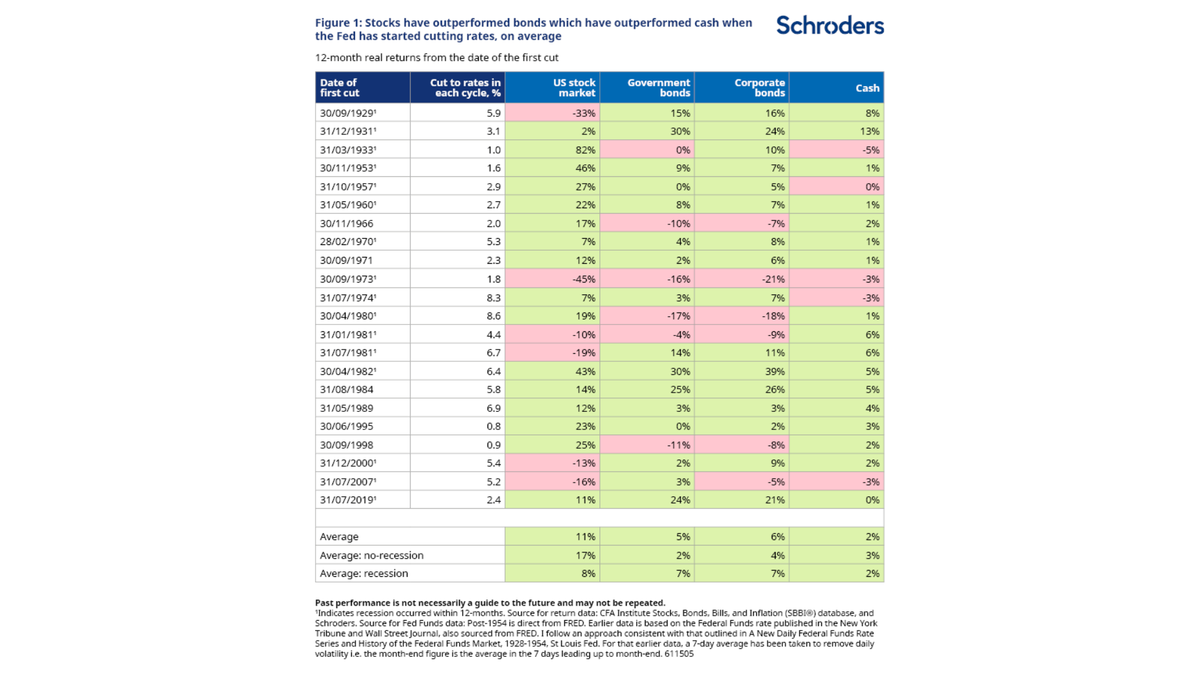

In the 12-months after the US Federal Reserve (“the Fed”) has started cutting interest rates, the average return from US stocks has been 11% ahead of inflation (Figure 1). They’ve outperformed government bonds by 6% and corporate bonds by 5%, on average.

Figure 1

Cash has been left further in their wake. Stocks have beaten cash by 9% in the 12 months after rates start to be cut, on average. Bonds have also been a better place to be than cash.

This is based on our new, long-term, analysis of investment returns during 22 US interest rate cutting cycles since 1928.

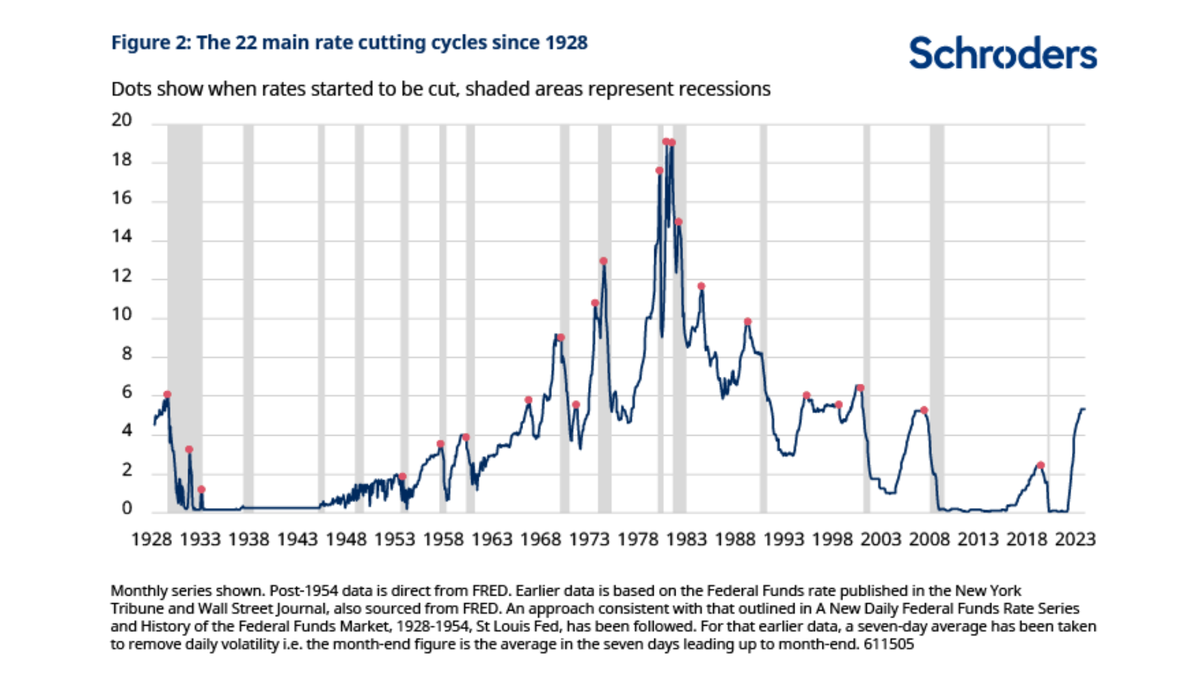

Figure 2

Stocks prefer if a recession can be avoided, but have usually coped ok even if one wasn’t

These returns are even more impressive considering that, in 16 of the 22 cycles, the US economy was either already in a recession when cuts commenced or entered one within 12 months (recession dates are marked in Figure 1 and shaded in Figure 2).

Stock returns were better if a recession was avoided but, even if it wasn’t, they were still positive on average (Figure 1).

There are big exceptions, and a recession is obviously not something to be welcomed but, for stock market investors, it has not always been something to unduly fear either.

Bond investors, in contrast, tend to do better if a recession occurs. They usually benefit from safe-haven buying (especially government bonds), which drives yields lower and bond prices higher. But they’ve also done ok if a recession was avoided. Corporate bonds have outperformed government bonds, on average, in this more economically-rosy scenario.

The range of historical returns is wide for stocks and bonds, but both have tended to do well when the Fed has started cutting rates.

What about today? Unlike most historical episodes, the Fed is not considering cutting rates because it’s worried that the economy is too weak. It is doing so because inflation is going in the right direction, meaning policy does not have to be so restrictive.

If it is right, and can engineer a “soft landing”, then 2024 could be a good year for stock market investors AND bond investors.