Another nerve-wracking week

By Holly Mackay, Founder & CEO

20 Mar, 2026

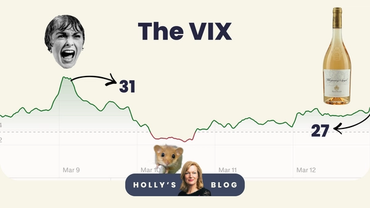

Yet another nerve-wracking week on markets. Wednesday was a day of wild swings as we digested the tit-for-tat strikes on Gulf energy infrastructure and what it means for both energy supplies and growth.

Most things I own slid about 2% yesterday. Pretty much everything apart from energy sold off and the FTSE 100 was down about 2.5%. Markets opened a little lower this morning, but things are stable. For now.

A quick note which will impact thousands of our readers. The UK’s largest broker, Hargreaves Lansdown has melted and been offline since yesterday afternoon, as far as I can tell. Ouch. You do not want to freeze people out of trading when markets are this volatile. I’m told there is no cyber security issue and client assets are safe, so no need for clients to feel any alarm – but it seems that there is no trading available as I write. Not good.

Back to markets, and this conflict is going to have long-term financial repercussions which – to me – seem to be underpriced by the markets currently. Supply chains are in chaos. The rapid end of the war we hear about seems difficult to believe. European actuaries are digging their heels in against Trump’s rhetoric when it comes to the costs of insuring vessels anywhere near the Strait of Hormuz. The going rate for insurance per tanker voyage is apparently up to $1 million. Gulp. But Trump’s plan to provide alternative, cheaper insurance though the Washington Development Finance Corporation is underfunded and not possible, according to J.P. Morgan calculations. So, it’s a mess.

And aside from the obvious hiatus in stock markets, inflation

and interest rates around the world are also reacting.Inflation is going up. Everywhere. As a result, central banks need to use their weapon in the inflation fight. Interest rates. Higher rates = less borrowing = less spending and hiring = lower inflation.

Over in the US, the Fed held interest rates steady this Wednesday, a move which was mirrored by the Bank of England on Thursday, as they agreed to hold rates at 3.75%. With oil prices remaining high (currently $110 a barrel as I write, which is about 50% higher than pre-war levels), there is no suggestion that inflation will come down any time soon. Which might yet see rates go up, rather than fall. You can read more here about what this means for your savings and mortgages.

Against this backdrop, another economic buzzword on everyone’s lips is stagflation

. Stagflation is a nasty beast. It rears its head at a time of sluggish economic (lack of) growth. At the same time as inflation is creeping higher.Normally anaemic economies go hand-in-hand with low inflation. Not much moves in a stagnant pond. But stagflation bucks this trend, and it’s not pleasant. The cost of living goes up as employment and economic activity falls.

HOWEVER. Despite all this hiatus, there are some things we can all do.

If possible, make sure you have something in cash, so you don’t need to be a forced seller of investments at any time of market volatility or lows.

If you’re a higher rate taxpayer, gilts are an interesting way to hold cash which won’t incur tax. I put some money into the Treasury Gilt maturing in October 2026, recently. This is basically an IOU to the Government. It cost me about £98 a unit, and I know I will get back £100 on 22 October this year. So that’s a certain return of a little over 2% in 6 months. Tax free. Won’t set the world on fire, but it’s better than a slap with a wet kipper or having to sit next to Pete Hegseth at dinner.

The end of the tax year is looming. With the tax take at all-time highs, we can and should use as much of our ISA allowances and pension allowances as possible. If you’re nervous about markets and not keen to jump in right now, you can always put the money into the account but leave it there as cash. We can all contribute up to £20,000 a year into a Stocks & Shares ISA, and many let us start with less than £100.

Higher rate taxpayers in particular do not forget about the power of a pension to reduce tax bills. Money you can shove into a pension will reduce next January’s tax bill.

Another cunning plan is to consider setting up a monthly direct debit or regular buy instruction. So rather than jump in now, dreading the next thing which might come out of Trump’s mouth, you can drip feed in little and often and smooth out your entry price.

Retirees. Don’t forget annuities, which are looking pretty good these days. These are products which let us swap a stack of retirement savings for a known annual payment – typically for as long as we live. These days, a singleton could trade in £100,000 for about £7,600 a year. For the rest of your life. You can have an annuity and also have other pensions too, which keep you invested. It’s not an either/or decision. And for gawd’s sakes, don’t just obediently take the one which your current pension company offers you. Shop around! I like the Government-backed MoneyHelper calculator for impartial quotes.

And an Inheritance Tax (IHT) nudge on the back of news this morning that IHT receipts hit £7.7 billion for April last year to February 2026. This is about £4 billion more than a decade ago. Sort a will and get some advice on any estate planning!

As for markets, I don’t pretend to have a crystal ball. I can't second guess what’s going to happen, but I don’t think it’s a quick fix. This week we spoke to some analysts about what to expect with the oil price spiking. But that cash buffer is super important, as is holding your nerve. Beginner investors who are not long in this game – don’t panic and sell up. You just lock in any paper losses, and things always come back. You just need to breathe through it. I promise!

Have a good weekend, everyone. The sun is shining, and it’s Friday. It could be a lot worse!

Holly

Post a comment:

This is an open discussion and does not represent the views of Boring Money. We want our communities to be welcoming and helpful. Spam, personal attacks and offensive language will not be tolerated. Posts may be deleted and repeat offenders blocked at our discretion.