Home • Articles • BoE Interest Rate Decision: How it Affects Your Savings, Mortgage, Pension and More

BoE Interest Rate Decision: How it Affects Your Savings, Mortgage, Pension and More

By Boring Money

1 May, 2026

The Bank of England (BoE) has kept the base rate at 3.75%. We explain what it all means for your money, whether you're hunting for the best savings rate, due for a remortgage, or weighing up your retirement options.

📉 What's happening with interest rates?

In Appril, members of the Bank's Monetary Policy Committee (MPC) voted to keep the rate at 3.75%.

Bank of England base rate, 2022 - present

The Bank's base rate is the interest

rate it charges banks and lenders when they borrow money. It’s essentially the UK’s benchmark borrowing cost, and it influences everything from mortgage rates to savings accounts.It's also the Bank’s main tool for controlling inflation

, which it aims to keep at a target of 2%.When inflation is high - meaning prices are rising too quickly - the Bank usually raises the base rate to encourage saving and reduce spending, which helps cool things down. When inflation is low or the economy is weak, the Bank may cut the base rate to stimulate borrowing and spending, giving growth a boost.

⬇️ What's happening with inflation?

UK inflation hit 3.3% in March 2026, up from 3% in February, and a long way from the Bank of England's 2% target. The next reading is due on 20 May. The US and Israeli attacks on Iran have lifted oil and gas prices, which is pushing inflation higher in the short-term. The long-term impact will depend on how long the Straits of Hormuz are closed and whether energy prices continue to rise. It is possible that there will be secondary effects as higher energy costs start to feed through into the prices of food and consumer goods. Against this backdrop, central banks across the world are choosing to wait and see.

💰 Savings: Clock is ticking on competitive rates

It's been good news for savers in recent years, having enjoyed competitive returns with easy-access and fixed-term savings products paying as much as 4.5%+. This had started to change, but as interest rate expectations have ticked higher, banks have started gradually to lift rates once again

Banks and building societies tend to align their cash savings products with the base rate, although they’re often a bit slower to react when there are changes (especially when it suits them).

Evidently, the usual advice is to shop around and make sure you're getting the best rate you can.

The savings environment remains attractive. Those looking to make their money work harder can access inflation-beating interest rates, with easy access Cash ISAs paying around 4-4.5% and fixed rate deals offering above 4.5%. There are also some short-term fixes of around six months on the market, offering savers a balance between returns and flexibility. If you’re looking to secure a longer-term fix, only commit money you can comfortably set aside and won’t need soon. A sensible approach can be to split your savings, locking away a portion to secure higher rates, while keeping some funds easily accessible for life’s unexpected twists and turns.

It pays to shop around for the best rate, rather than defaulting to your high street bank. If you already have existing savings, it’s worth checking the rate you’re getting is competitive. Tucking cash savings into a Cash ISA will shield your returns from income tax today and in the long run.

🏡 Mortgages

The Bank's decision to keep the base rate to 3.75% is potentially good news for homeowners who may have been fearing a rise in the face of higher inflation. However, far more important for mortgage prices is the government bond yield

, which remains higher than the base rates. Lower fixed rate deals have been disappearing from the market.📉 Tracker mortgages

Tracker rates have been gradually closing the gap on fixed rate options, but are still behind the best of the fixes. With rate cuts off the table until the crisis is over, more borrowers may see fixed rates as a better option.

Trackers have some advantages. They are also more likely to be free of any early repayment charge which gives added flexibility. However, there’s no guarantee that rates will continue to drop, and so borrowers need to have some ability to cope with rising payments if rates take a turn.

🌀 Variable rate mortgages

Standard variable rate (SVR) mortgages aren’t directly tied to the base rate, but most lenders follow the Bank’s lead. Around 600,000 homeowners in the UK have an SVR deal, and the current best rates are 4.1%[6]. If the base rate is cut later in the year, this should be reflected in lower variable rates - just bear in mind that SVRs are typically higher than most fixed deals, and lenders can be notoriously sluggish about passing on cuts.

🔒 Fixed rate mortgages

Until recently, fixed rates had come down significantly and there was a wealth of sub-4% options. However, these have gradually been withdrawn as inflation and interest rate expectations have moved.

Even though the base rate hasn’t moved, mortgage rates have lurched higher. Swap rates, which reflect where markets think borrowing costs are heading and help determine the pricing of home loans, have risen again. Their direction from here will be influenced by how the Iran conflict evolves and its impact on inflation.

Fears of higher interest rates at the outbreak of war two months ago ramped rates up, but more recently those fears have eased slightly. It means we’ve seen mortgage rates rise and then fall back.

Disappointment with the lack of progress with peace talks, plus higher oil prices, mean swap rates are up, which could mean mortgage rates rise again. With so much uncertainty over what happens next in the Middle East, this isn’t guaranteed either, so it’s worth hedging your bets.

If you have a remortgage due in the next six months, check if you can agree a deal for your remortgage now. If rates fall from here, you can shop around elsewhere, but if they rise, you’ll have locked in a competitive rate.

A fixed rate may be more attractive to remortgagers in such an uncertain environment. However, given how these rates have risen, some people may opt for a shorter fix, in the hope the immediate crisis has passed by the time they come to remortgage again.

👵 Pensions & annuities: Rates still at record highs

Higher interest rates over the past few years have helped push annuity rates to their highest levels in over a decade. That’s been a rare slice of good news for retirees looking to lock in a guaranteed income for life. Annuity rates are likely to remain high for the time being.

Best annuity rates, April 2026

Annuity rate and income – single life annuity

Age | Annual Income | Annuity rate | Provider |

55 years | £6,616.80 | 6.62% | Legal & General |

60 years | £6,932.16 | 6.93% | Aviva |

65 years | £7,626.84 | 7.63% | Canada Life |

70 years | £8,425.80 | 8.43% | Legal & General |

75 years | £9,678.84 | 9.68% | Legal & General |

Source: Retirement Line, Hargreaves Lansdown. April 1st, 2026.

If you're approaching retirement and considering an annuity, it would be wise to shop around and start getting quotes well in advance. This will give you the best chance of securing the best possible rate on your retirement savings.

It's also worth remembering that annuities aren't your only option and that you can even opt to blend one with a drawdown strategy to maximise your income:

From an annuity perspective, the picture is more nuanced than the Bank Rate alone. Annuity pricing is driven largely by long-term government gilt yields – effectively the cost of government borrowing – which remain close to their highest levels since the 2008 financial crisis, even after six interest rate cuts since 2024.

With the Bank of England voting to hold rates today and the government’s borrowing costs hitting recent highs, those considering an annuity can continue to benefit from a competitive pricing environment…With the full impact of the geopolitical backdrop yet to be realised, uncertainty remains a defining feature of today’s market. In this environment, the security of a guaranteed income can look increasingly appealing to retirees who value certainty and stability.

If you're considering purchasing an annuity, contact a professional annuity broker or financial adviser before committing yourself to anything. They can help you filter options best suited to your individual circumstances.

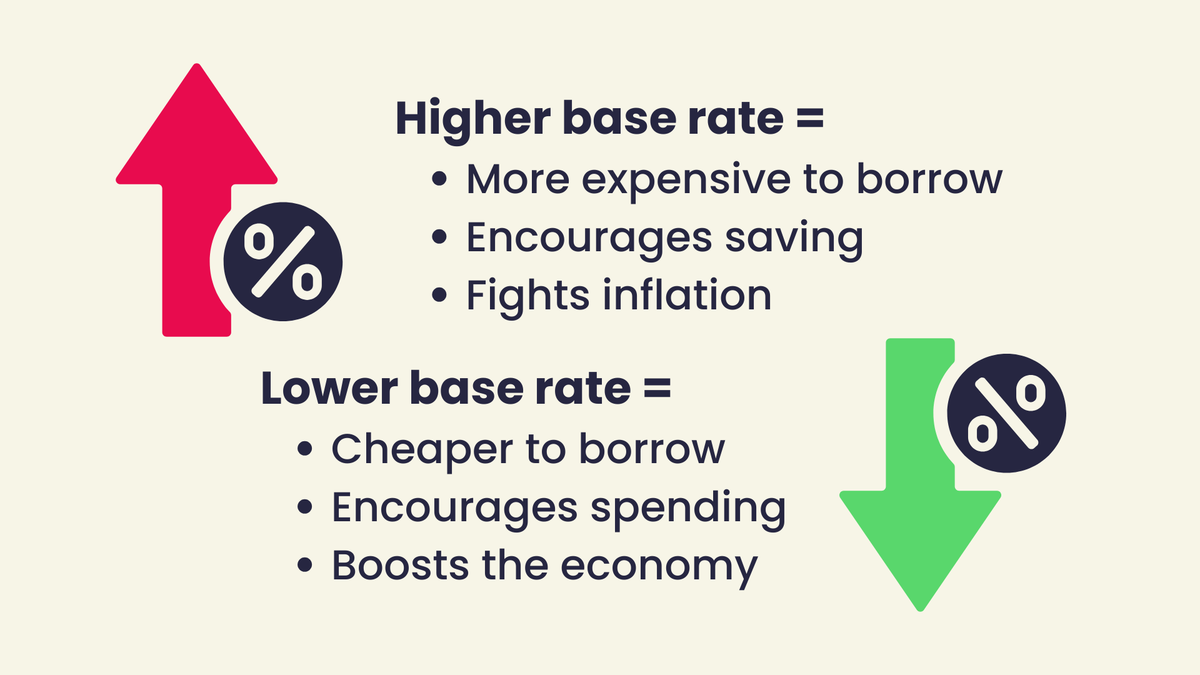

🎯 The bottom line

Here are the key takeaways of what you need to know about your mortgage, savings, and pension pot in light of the Bank's decision:

🤔 So what should you do?

---

[1] House of Commons, July 2024

[2] Office for National Statistics, September 2025

[3] Deutsche Bank UK, September 2025

[4] MHA, August 2025

Post a comment:

This is an open discussion and does not represent the views of Boring Money. We want our communities to be welcoming and helpful. Spam, personal attacks and offensive language will not be tolerated. Posts may be deleted and repeat offenders blocked at our discretion.