Behind the Scenes at Quilter Invest: Where Old Wealth Meets New Tech

By Boring Money

21 Nov, 2025

This section is a paid promotion created in partnership with Quilter Invest. The views and information presented reflect the sponsor’s messaging and may not represent the independent opinions of Boring Money. While we aim to ensure accuracy and relevance, this content should not be considered impartial advice.

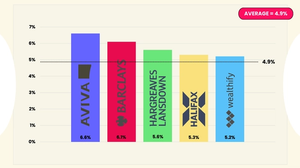

Last quarter, we released our best performing ready-made solutions of July-September 2025, and Quilter Invest topped the charts. On the back of this, we had a few readers asking for more information about who Quilter Invest is – so here's some background.

What drives the performance of their ready made performance?

Our investment performance is underpinned by our forward-looking strategic asset allocation (“SAA”), which analyses a wide range of economic indicators to determine the most favourable investments. We diversify risk by adopting a multi-asset approach, putting our customers' assets in many baskets rather than one. This approach provides good customer outcomes by seeking to deliver strong returns with appropriate risk.

The wealth management giant's digital transformation aims to bridge Britain's advice gap – but can a heritage brand truly disrupt?

When a FTSE 250 wealth manager with roots stretching back 250 years acquires a scrappy fintech startup, eyebrows tend to rise. Yet that's precisely what happened in September 2024 when Quilter plc purchased NuWealth (formerly Wombat Invest) to bolster its digital credentials.

Fast forward to October 2025, and NuWealth has been rebranded as Quilter Invest, marking the wealth manager's most visible play yet for younger, digitally-native investors who aren't quite ready for traditional financial advice. But beneath the shiny app interface and £10 minimum investment lies a more complex story about Britain's wealth management industry and the regulatory pressures reshaping it.

From Coffee Houses to Mobile Apps

Quilter's journey to digital investing is anything but straightforward. The earliest predecessor firm was established as a partnership of stockbrokers at Jonathan's Coffee House in the 1700s. Through successive acquisitions – including Skandia (acquired by Old Mutual in 2006) and a half-billion-pound platform upgrade completed in 2021 – the business eventually rebranded as Quilter plc in 2018.

The company now manages £126 billion in assets, serving over 500,000 clients through 8,000 financial advisers. Yet traditional wealth management faces an existential challenge: UK financial advisers have declined to approximately 35,000, while 11 million Britons hold between £50,000 and £5 million in investible wealth – many needing guidance but lacking access to it.

Enter the "advice gap" – and Quilter's rationale for acquiring NuWealth.

As expectations for digital engagement evolve, we see a clear opportunity to close the advice gap for people who need some guidance but aren’t ready for full financial advice. The NuWealth acquisition gave us a scalable way to help those at the start of their investing journey, highlight the benefits of advice, and prepare for future regulatory changes.

The Digital Proposition

Quilter Invest positions itself firmly at the entry point of the investment journey. The My Goal fund range provides access to ready made portfolios, allowing for an easy hassle free route to investing. The platform also offers fractional shares in companies like Apple, Tesla, and Amazon, themed funds ("Pure Gold," "The Techie," "The Green Machine"), and tax-efficient wrappers including ISAs and Junior ISAs – all accessible with as little as £10.

The pricing is deliberately straightforward: £2 monthly covers all investment accounts, plus a 0.25% annual platform fee. Fund provider fees range from 0.07% to 0.75%, with a 0.40% FX fee on foreign shares. The app emphasises education through a Learning Hub with courses and articles designed for beginners, supported by UK-based customer service. You can open an account for free, allowing customers to look around and try the app before investing. Once invested, the £2 monthly fee covers all investment accounts and allows unlimited trading across their range of funds, ETFs, and shares.

But Quilter Invest's real differentiation isn't the technology – plenty of apps offer fractional shares. It's the institutional backing and integration pathway into full financial advice.

The Regulatory Tailwind

Timing matters. Quilter's acquisition arrived just as the FCA's "Targeted Support" proposals moved towards reality, creating a middle ground between pure information and full regulated advice – precisely where Quilter Invest operates.

Quilter have been explicit about this positioning:

The platform serves clients who fall between guidance and full advice, offering a simple, accessible way to start investing, with the flexibility to transition into advised services.

This creates a compelling flywheel for Quilter's business model. Financial advisers can use Quilter Invest to engage "pre-advice" clients: adult children of existing clients or individuals not yet ready for the £50,000-£250,000 minimums traditional advisers require. As portfolios grow and life becomes more complex, the natural transition point beckons towards full advice – preferably delivered by a Quilter adviser, with assets on the Quilter platform.

Quilter Invest is designed to complement our advice offering. It gives advisers a way to engage those who aren’t ready for full advice today but will need it as their circumstances evolve. By integrating digital investing with our platform and advice network, we create a natural progression from self-directed investing to holistic financial planning. This strengthens adviser relationships, supports long-term client outcomes.

Quilter Invest is focused on supporting customers take their first steps in their investing journey. It provides learning, guidance and a simple investment range, as well as an easy route to financial advice. We are not necessarily competing with the large D2C players and our competitive pricing reflects that.

What's Actually Different?

Strip away the marketing and a fundamental question emerges: does Quilter Invest represent genuine innovation, or simply a defensive response to digital disruption?

The honest answer sits somewhere between. Quilter isn't reinventing investment products. The app offers competent execution of digital investing table stakes: fractional shares, thematic funds, low minimums, educational content, and tax wrappers.

What's potentially distinctive is the integration play – creating a coherent client journey from £10 first investments through to six-figure discretionary portfolios within one ecosystem. Whether that delivers superior outcomes for customers remains to be demonstrated.

There's also an intriguing philosophical tension. Quilter's heritage businesses emphasise active management, bespoke portfolios, and premium service. Quilter Invest, by necessity of its price point, must lean on passive index funds and automated processes. Bridging that divide whilst maintaining brand coherence poses unique challenges.

With Quilter Invest we want to help more people in the UK start and grow their wealth. We want to be a clear option for anyone beginning their investing journey, with the flexibility to evolve as life becomes more complex. By combining intuitive digital tools with access to advice when it’s needed, we aim to create a continuum of support that helps customers make confident decisions and achieve better outcomes over the long term.

The Verdict

Quilter Invest represents a calculated bet that Britain's advice gap can be addressed by established players embracing digital-first distribution. The regulatory tailwind from Targeted Support proposals provides momentum, and integration within Quilter's ecosystem offers differentiation from pure-play competitors.

But success is far from guaranteed. Digital platforms face intense competition, thin margins, and fickle customer loyalty. Quilter must operate with startup agility whilst leveraging institutional advantages – a balance many incumbents fail to strike.

For consumers, Quilter Invest offers a credible entry point backed by FCA regulation, FSCS protection, and substantial resources. The educational content appears genuine, and fees are competitive if not market-leading.

Whether it becomes a genuine bridge across the advice gap or simply another competent investing app likely depends on execution over the next few years – and whether regulatory changes genuinely create space for the "targeted support" model Quilter is positioning to fill.

One thing is certain: the next chapter in this 250-year-old firm's history will be written in code, not ledgers.

Success for Quilter Invest means more than launching an app – it’s about changing behaviours and making investing accessible to everyone. We want to remove barriers, build confidence, and create a pathway that supports people throughout their financial lives.

Capital at risk. This article is for informational purposes only and does not constitute financial advice.