Do Geopolitics Really Matter for Your Investment Portfolio?

Written by Boring Money

6 Feb, 2026

Geopolitical tensions are having increasingly significant impacts on investment returns as the post-war consensus of globalisation and free trade gives way to resource nationalism, tariffs, and government intervention. The weakening dollar cost UK investors 8 percentage points of S&P 500 returns in 2025, while gold has surged over 90% as its safe haven status eclipses US treasuries. US-China AI rivalry is driving big investment in semiconductors through initiatives like the $280 billion Chips and Science Act, reshaping the technology sector. Major economies, including the US, UK, Italy, France, and Canada, now have debt-to-GDP ratios

exceeding 100%, making bond markets vulnerable to perceptions of government stability. While traditional studies suggest geopolitical events have temporary market impacts, the current environment of direct government intervention in companies and sectors—from tariff threats to Trump administration pressure on oil majors—is creating more lasting effects that investors cannot ignore.

The received wisdom is that geopolitics don't matter for investment returns in the longer term. International tensions can create temporary blips in, say, the oil price, or specific companies, but in the long run, they do not materially affect the price of companies or of investor returns. However, these assumptions may need to be challenged as the environment changes.

Why traditional views on geopolitics and markets are changing

Most studies looking at the relationship of geopolitics and stock markets were set against the post-war consensus and a broader backdrop of globalisation, free trade, and generally benign relationships between major countries. Today, there is a new brand of geopolitics, involving resource nationalism and tariffs. The potential for it to spill over into investor returns has already been seen in 2025, and its impact may be even more acute in 2026.

The US is fundamentally reshaping its economic and geopolitical relationships with the world, as reflected in its recently released National Security Strategy. The Administration's approach to trade, industrial policy, government intervention into the private sector, and alliances and partnerships marks a decisive break from the post-Cold War order and the US's role therein.

This has been evident in the early weeks of 2026. The Trump administration has intervened in Venezuela and is threatening strikes on Iran. Having disrupted markets with the announcement of his 'liberation day' tariffs in 2025, the President has sought to use tariffs as a tool of international pressure again in 2026, notably against Canada and Europe.

How Geopolitics Affects Currency Markets

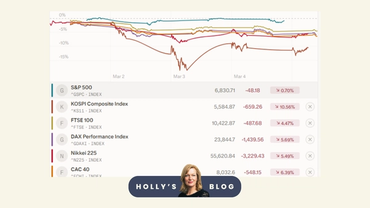

Last year, one of the biggest impacts from geopolitics was the weakening of the Dollar. This affected returns to UK investors from Dollar assets

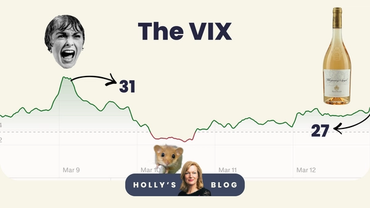

. For example, while the S&P 500 rose 17.9% in USD terms, unhedged UK investors would have received just 9.8% over the year. The Dollar has lurched lower again over the past two weeks in response to US foreign policy interventions.If these geopolitical interventions continue to diminish investors' faith in US assets, the impact could be significant. At the extreme, it could prompt ructions in the bond market that would be destabilising for all stock markets.

There is a changing perception on the USD and US treasuries as a safe haven asset. Its status is eroding.

The weakness of the Dollar has an impact on other currencies. It can provide a boost to other 'safe haven' currencies – the Swiss franc, for example – though for the time being, gold and other precious metals appear to have been the strongest beneficiary. If the weakness continues, it will affect the relative attractiveness of US assets.

Artificial intelligence: The new geopolitical battleground

Artificial intelligence has become the new space race. BlackRock points out that US-China rivalry remains the defining feature of geopolitics with competition across trade, technology, energy, and defence, but it adds:

Artificial intelligence is at its core. Both countries view AI as central to future economic and military advantage, and both are working to reduce dependencies that could be used for leverage in a prolonged era of competition.

This has created significant rivalry over the semiconductors used to power AI. Access to chips means that the US has to care what is happening in Taiwan, for example, which is home to the world's largest chipmaker, TSMC. The US has sought to support its domestic chip industry. The 2022 Chips and Science Act allocated approximately $280 billion to boost domestic research and manufacturing of semiconductors. It has also sought to restrict exports of chips to China, placing tariffs on exports of Nvidia's valuable H200 AI processor chip. At the same time, China is seeking to build self-reliance in AI. This rivalry is likely to support the AI sector as a whole and the ecosystem that supports it.

Commodities: Gold, Oil, and Geopolitical Hedges

Recent research from Allianz Global Investors looking at the relationship between financial markets and geopolitics found that markets don't follow the same pattern after geopolitical events, but the exceptions are the US Dollar and gold – "both tend to strengthen in the year after a geopolitical event," says Stefan Hofrichter, head of global economics & strategy at the group.

While this hasn't been true for the Dollar this time round, it has certainly been true for gold in the current cycle. The gold price is up over 74% over the past 12 months. It has become the go-to safe haven for investors worried about erratic policymaking from the US and mounting geopolitical tensions. There are no signs of this fading, with the gold price spiking in response to both the Iran and Venezuela interventions since the start of the year.

Why oil prices respond differently to geopolitical events

The oil price has a complicated relationship with geopolitics. It is often at the heart of geopolitical tensions, and oil price spikes can ripple through inflation data, as they did in 2022 with the Russia/Ukraine crisis. However, oil price spikes in response to geopolitics are often short-lived in nature.

Perhaps unsurprisingly, many of the occasions when oil prices have continued to rise more than three months after a geopolitical event are when it has been in the Middle East, one of the world's largest oil-producing regions. Yet none of the three biggest rises in oil prices we tracked have been in the past 25 years. We think this may partly be because the world is better able to cope with the threat of disruption to oil supplies these days. Many countries have broadened their suppliers of oil since the 1970s energy crisis. And the world has become less dependent on hydrocarbons, shifting more of its power to sustainable sources.

This has been evident with the recent US interventions in Venezuela and Iran. These incursions have had little enduring impact on the oil supply. The oil price has remained depressed, with investors still nervous about a potential supply glut.

Nevertheless, commodities have provided one of the most enduring hedges against geopolitical tension. Gold has generally protected against currency debasement, while mining groups were one of the few areas to defend capital in the rocky markets of 2022.

Bond markets and sovereign debt concerns

Part of the problem for policymakers has been the vast debt held by major powers. Japan, France, Italy, Canada, and the US all have a debt-to-GDP ratio of over 100%. This leaves them vulnerable to perceptions on the reliability or otherwise of government decision-making. Japan has been at the forefront of this, with spikes in long-dated Japanese government bonds in response to rising debt levels.

Over the past year, we have seen a revolving door, where investors get worried about the fiscal sustainability of an individual country. This is going to be a very concerning issue for many countries, with fiscal budgets a big problem. Bond investors are going to be on the sidelines and will be increasingly discerning, punishing bonds on the long end.

Geopolitical tensions could prove important to the extent that they create concerns about a country's stability and move its borrowing costs.

Do geopolitics really matter for equity markets?

Geopolitics should matter less to equity markets.

While geopolitics can cause short-term market jitters, company fundamentals are the true north for long-term investors.

He points to a study by J.P. Morgan analysing over 80 years of data that showed while geopolitical events can have profound impacts on local markets, they rarely have lasting effects on large-cap equity returns.

The study showed that six months to a year after a geopolitical event, market returns are often indistinguishable from periods without such events.

The "Visible Hand": Government intervention in markets

However, Hooper says that she is increasingly seeing evidence of the "visible hand" in markets. Initially, this was evident in tariff threats, which weighed significantly on certain sectors – consumer staples, for example, or pharmaceuticals, that rely on relatively open markets to distribute their products.

Now it is also evident in the US government's intervention in individual companies. Hooper points to the Trump administration's discussion with the oil majors, pushing them to invest in Venezuela. There were also moves to cap credit card interest rates at 10%. This could have seen many people with low credit scores losing access to credit cards. Intervention by JP Morgan Chase CEO Jamie Dimon, who said the move would be a 'disaster', was followed by $5bn law suit against him for an alleged 'debanking' of the Trump family.

What This Means for Your Portfolio

Geopolitics can matter and are becoming increasingly important as a new world order is established. They can be a source of risk, but also opportunities, as asset prices exhibit volatility. They cannot drive investment selection, but neither can investors ignore them.

Frequently Asked Questions

How do geopolitical events affect investment returns?

While traditional studies suggest geopolitical events create only temporary market impacts, the current environment of resource nationalism, tariffs and government intervention is creating more lasting effects. Currency movements, commodity prices and sector-specific impacts can significantly affect portfolio returns.

Why is the US dollar weakening?

The dollar has weakened due to diminishing investor faith in US assets amid foreign policy interventions and mounting government debt. The US debt-to-GDP ratio exceeds 100%, and geopolitical actions have eroded the dollar's traditional safe haven status, with investors shifting to gold instead.

How does the US-China AI rivalry affect investors?

The AI competition between the US and China is driving significant investment in semiconductors, domestic chip manufacturing, and AI infrastructure. The US's $280 billion Chips and Science Act and export restrictions on processors like Nvidia's H200 chip are reshaping the technology sector and creating long-term opportunities.

Should I invest in gold during geopolitical tensions?

Gold has proven to be a reliable hedge, rising over 90% in the past 12 months. Research shows gold typically strengthens after geopolitical events, unlike other assets. With ongoing tensions and concerns about currency debasement, gold remains attractive as a safe haven asset.

Do geopolitical events have lasting effects on stock markets?

J.P. Morgan research analysing 80+ years of data shows that while geopolitical events can cause short-term volatility, returns typically normalize within 6-12 months for large-cap equities. However, government intervention through tariffs and sector-specific policies can create more persistent impacts on certain industries.