Investing without an adviser just got a lot less daunting

Written by Boring Money

2 June, 2026

Sponsored by Quilter Invest

This section is a paid promotion created in partnership with Quilter Invest. The views and information presented reflect the sponsor’s messaging and may not represent the independent opinions of Boring Money. While we aim to ensure accuracy and relevance, this content should not be considered impartial advice.

More people are investing than ever before. According to Boring Money’s 2026 research, 20% of UK adults now hold a Stocks & Shares ISA, up from 17% in January 2025 and 13% in 2020. Progress, clearly. But that still means eight in ten adults don’t have one.

The question is why. And a big part of the answer comes down to confidence, and a gap in the support available to people who aren’t ready to go it alone, but don’t need (or can’t afford) full financial advice.

When we ran a reader survey last year, we described three types of investment service in plain English: going it entirely alone (DIY), getting full financial advice (Do It For Me), and a middle option, guidance based on your situation, with no advice fee attached. We called it “People Like Me.”

The response? Confusion. Readers struggled to understand what that middle option was or whether they could trust it. And yet when we explained it properly, it was the option most people said they’d want.

It turns out that “People Like Me”, now officially called targeted support, is one of the most misunderstood developments in UK investing right now. Which is a problem, because it might also be one of the most useful.

So what actually is targeted support?

The FCA has been working to close what’s often called the “advice gap”, the gulf between people who can afford a financial adviser and people who are left entirely on their own. The scale of it is significant: according to Boring Money’s Advice Report, an estimated 12.3 million UK adults are currently in the advice gap. Targeted support has the potential to lift up to 5.9 million of them out of it.

Who are these people? Three in four have less than £50,000 in assets, which for many makes traditional financial advice difficult to access or justify financially. And the majority say they’d prefer a free solution that provides suggestions based on their financial characteristics over paying for personalised recommendations.

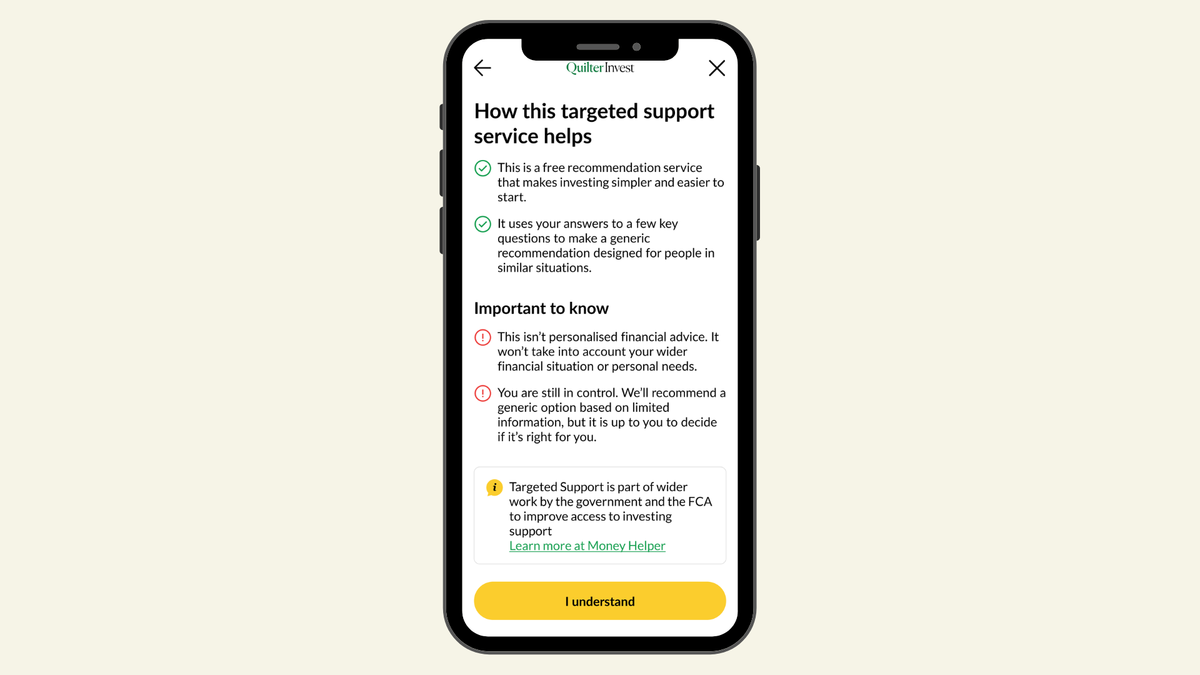

Targeted support is designed precisely for them. It’s not financial advice. It doesn’t take your whole financial picture into account. But it does ask you enough about your situation to point you in a sensible direction, and it’s free.

Think of it less like consulting an adviser, and more like a very well-designed set of signposts. Based on your answers, it can tell you what kind of investment might suit people in a similar situation to yours.

Quilter Invest is one of the first to do it

Targeted support has been discussed in policy circles for a while. Actually building and launching it, is another matter. Quilter Invest is among the first providers to have done exactly that, with a live, in-app targeted support journey available to their customers right now.

As Steven Levin, CEO of Quilter, explains:

While holistic advice is often the right solution for those with more complex financial needs or multiple objectives, we recognise that not everyone requires or wants it. Too often, that leaves people facing important financial decisions on their own. We believe in providing the right support at the right time to help people achieve brighter financial futures.

The journey lives inside the Quilter Invest app. It takes around 4–5 minutes, asks 9 questions, and ends with a fund recommendation matched to your situation. It’s free for all Quilter Invest clients.

What does the journey actually look like?

Here’s where it gets interesting, because the questions are carefully designed to build your confidence, not just tick compliance boxes.

Before you even get to the questions, the app walks you through a short educational sequence.

It’s a quick grounding in why investing matters, inflation eroding cash savings, the value of starting early, the snowball effect of compound growth. The kind of context that tends to get lost when someone is just handed a fund list.

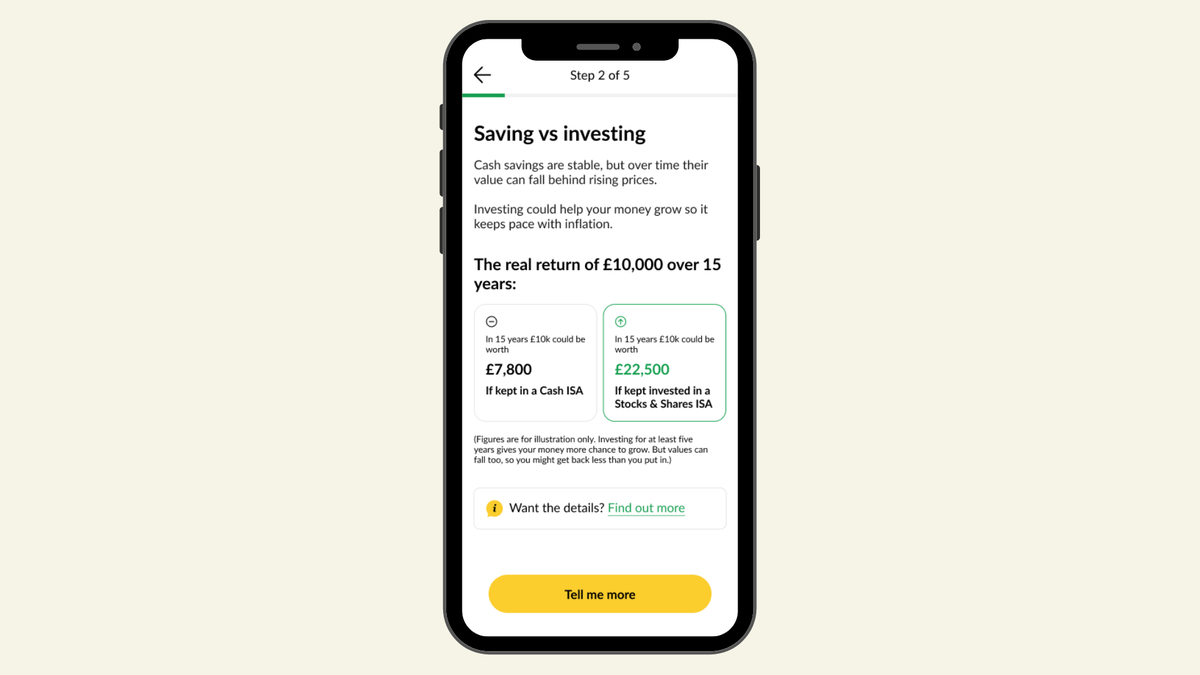

This screen makes the case plainly: £10,000 kept in cash over 15 years could be worth £7,800 in real terms. The same amount invested could be worth £22,500. Those figures are illustrative, but the direction of travel is real, and it’s exactly the kind of comparison that makes people stop and think.

Then, once you’ve got the context, the questions begin.

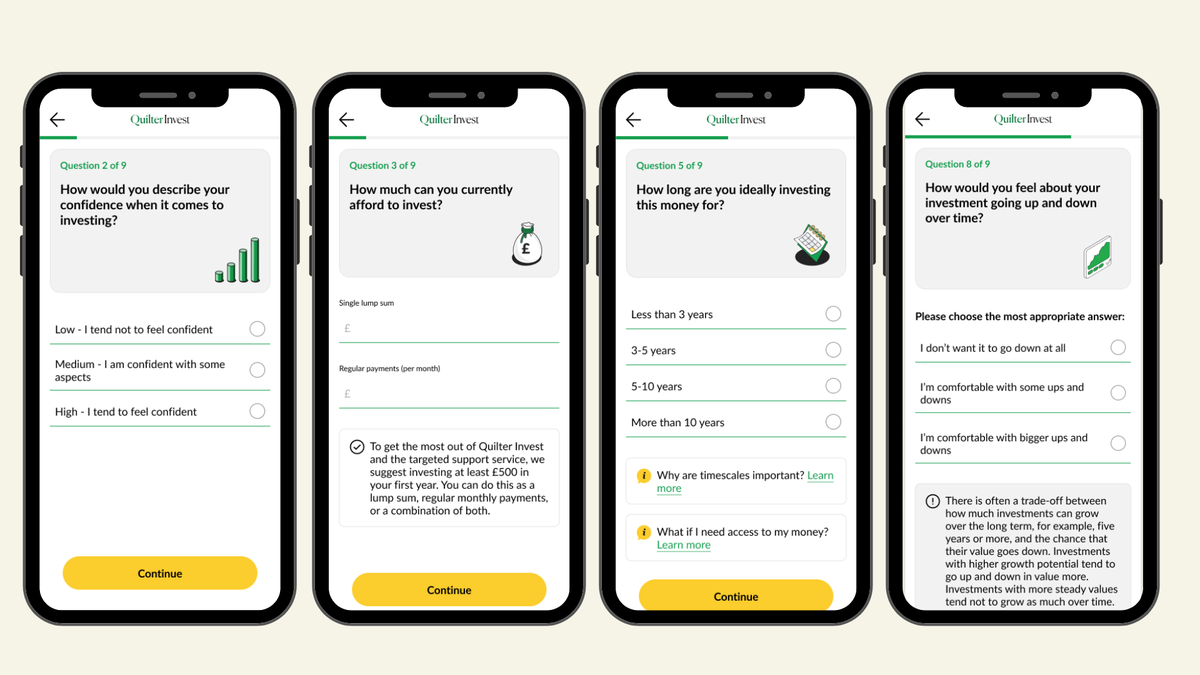

The 9 questions cover:

Your experience and confidence with investing

How much you’re looking to invest (lump sum, regular payments, or both, with a suggested minimum of £500 in year one)

How long are you planning to invest for

Whether you’ve already used your ISA allowance this tax year

How would you feel about your investment going up and down in value

Each question includes a brief explanation of why it matters, which again is the detail that tends to get skipped in a standard application form. The timescale question, for example, includes a “Why are timescales important?” explainer right there in the screen.

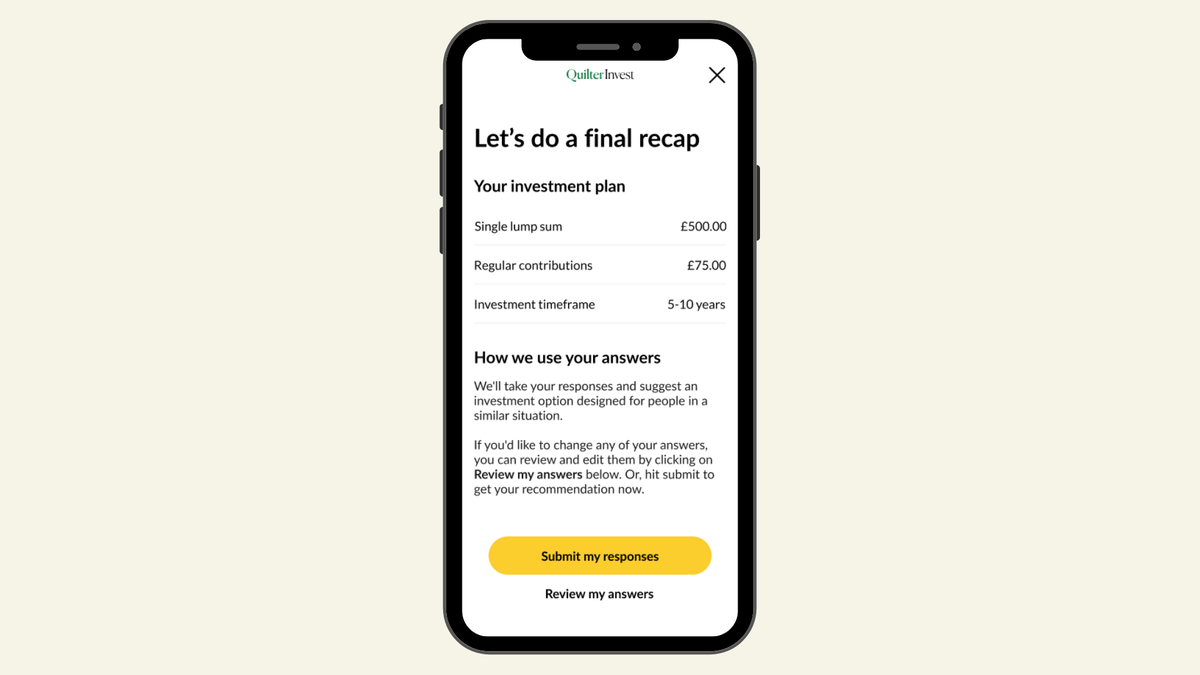

Before submitting, you get a recap of your investment plan, lump sum, regular contributions, and timeframe, and the chance to review your answers.

What you get at the end

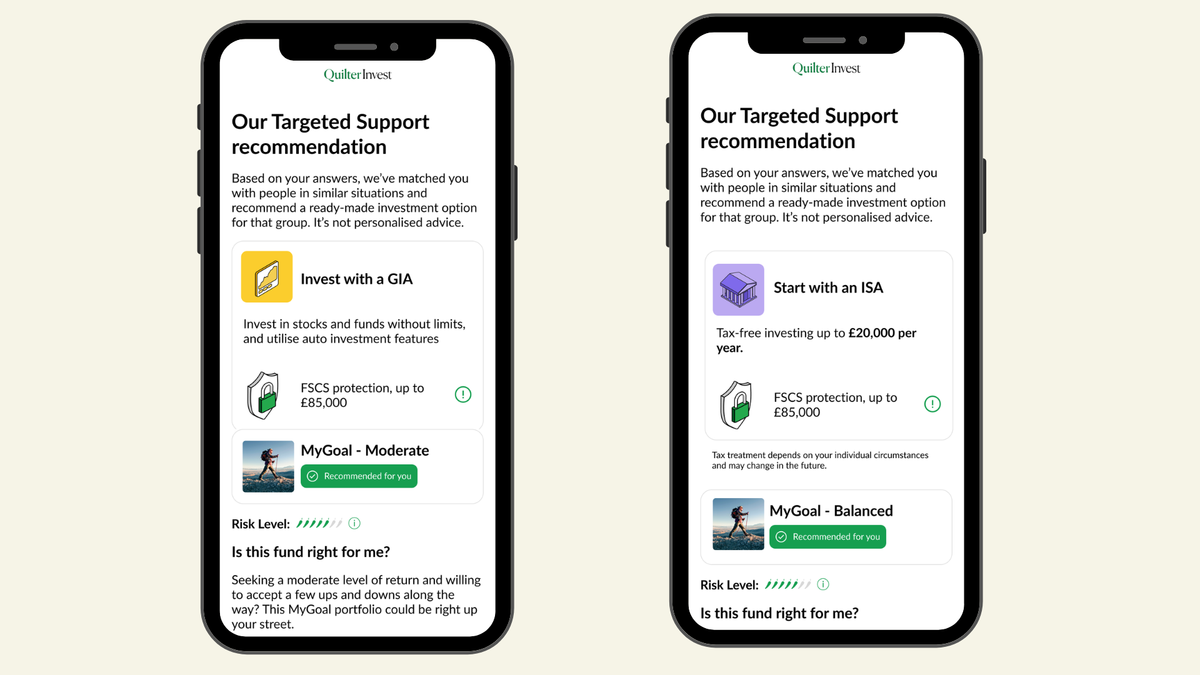

Based on your answers, the tool matches you to one of four Quilter MyGoal managed funds, and recommends whether to hold it in an ISA or a General Investment Account (GIA), depending on your ISA allowance situation.

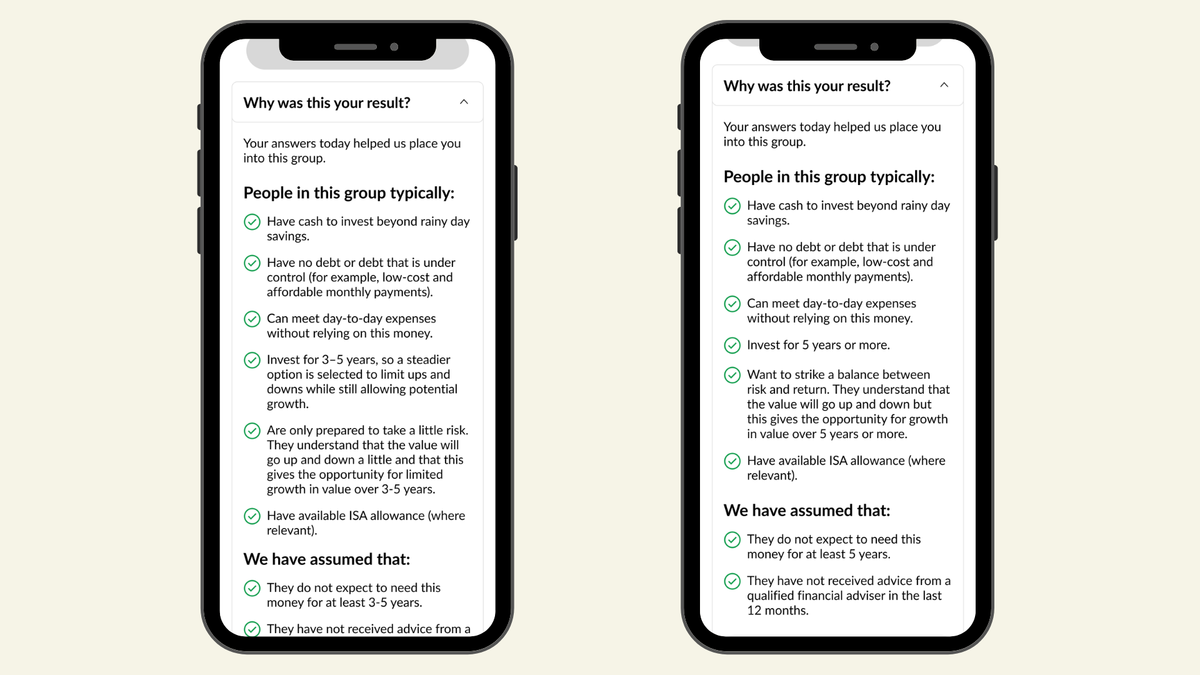

The recommendation page is detailed but readable. It shows you your matched fund, the risk level, projected growth figures (illustrative), and, importantly, explains why this was your result. The “people in this group typically” section is where the “people like me” idea becomes tangible. You’re not just given a fund. You’re shown who you’re being compared to, what assumptions were made, and what the costs will be.

As Kane Harrison, CEO of Quilter Invest, puts it:

Investing can feel intimidating, particularly if you’re new to it and don’t know where to start. Not everyone needs full financial advice, but that doesn’t mean they should be left to figure everything out on their own. By asking a few simple questions and providing guidance that reflects someone’s circumstances and attitude to risk, our new targeted support service helps people decide whether investing is right for them and, if it is, how to get started with greater confidence.

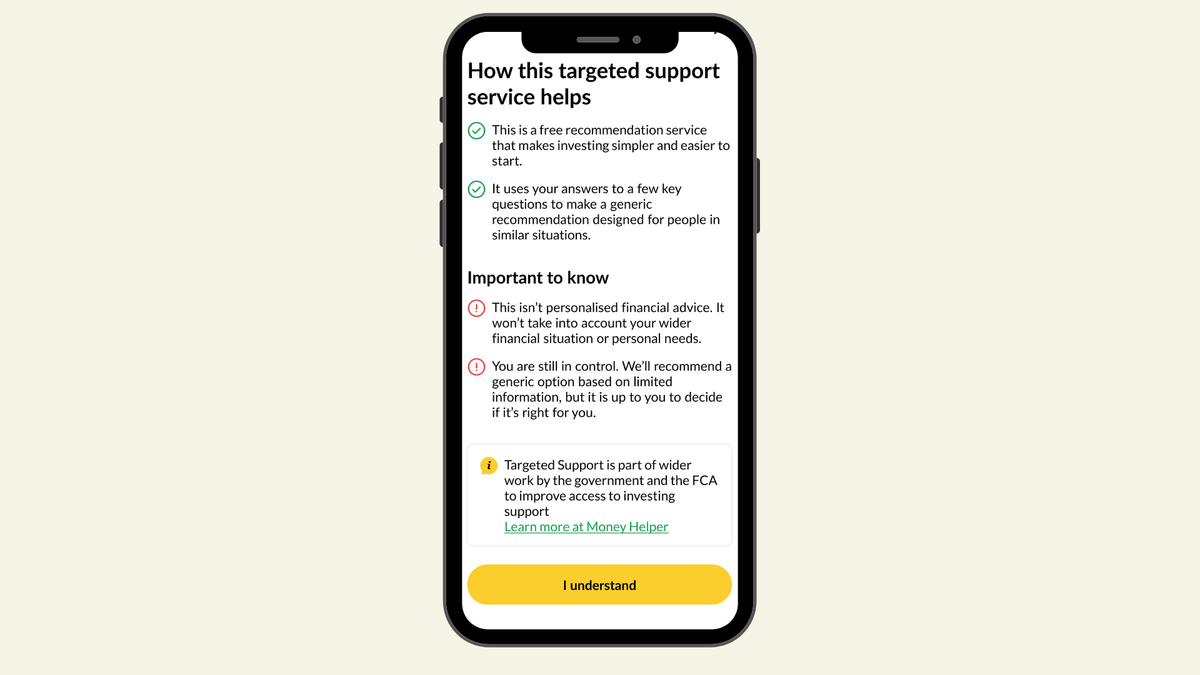

What it doesn’t do, and why that matters

Targeted support is not personalised financial advice. It’s important to be clear about that. It doesn’t take your whole financial situation into account, and it won’t replace a full fact-find or holistic financial plan. The recommendation is based on limited information. The app says so explicitly.

That transparency is reassuring rather than off-putting. The service is honest about what it is and isn’t, and it puts you in control of the final decision.

For people with straightforward situations who want a starting point, not a full plan, that’s exactly the right framing.

The bigger picture

Changes to cash ISA rules, a government push to get more people investing, and ongoing FCA (Financial Conduct Authority) work to improve access to financial guidance are all converging right now. Targeted support is part of that shift, and Quilter Invest is ahead of the curve in having something live and working.

If you’ve been sitting on the investing fence because you didn’t want to pay for advice but weren’t confident going it alone, this is precisely the kind of service that’s been built for you.