From Black Holes to Bubbles

By Holly Mackay, Founder & CEO

21 Nov, 2025

Another week, another Budget rumour. I’m not going to comment any more on the spin and speculation and will wait for the actual event next Wednesday. Gone are the days of the boring Budgets, when you could pop to Pret in the middle for a sandwich and not miss much!

Last week I gave a talk about economics and money in a sixth form college. When I told them that alcohol was banned in the House of Commons chamber with the exception of the Chancellor whilst giving the Budget speech, they were amazed. Older readers may recall Ken Clarke sipping a whisky and Geoffrey Howe having a gin & tonic. Even older readers will recall that Disraeli had brandy and Gladstone quaffed sherry and a beaten egg. 😉

I can’t see Rachel Reeves indulging but if she did… what would it be? To my delight there is a cocktail called ‘Black Hole’ which is the revolting-sounding mix of black sambuca topped with soda. If you’re going to announce tough news, you may as well do it with panache?

We will be bringing you a round-up at the end of the day next Wednesday. We’re also hosting a webinar with RBC Wealth Management to take all of your questions at lunchtime on Monday, 1st December – sign up to watch live or on catch-up and submit questions in advance.

From Black Holes to Bubbles

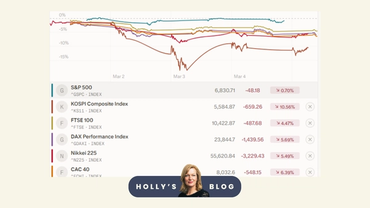

The other big question continues to be the ‘will it won’t it?’ question of tech markets and bubbles. Nvidia’s outstanding results this week confirmed that it had increased sales of chips at a faster rate than predicted, as the world’s most valuable company reported more than a 60% increase in sales for the 3 months to the end of October. Their estimated revenue for the last three months of 2025 alone is $65 billion.

Despite some volatility as I write, to some degree, these amazing results flicked the Vs at the bears who had been selling off tech stocks in recent weeks. But on the other hand, stocks are on course for their worst week since April, and we are seeing some unsettling swings. Investors are scratching their heads, trying to work out if this is a short-term clear out before a seasonal Santa Rally, or whether a bubble is about to burst. Whatever your view, it’s a reminder of how AI’s bright lights can blind most of us to the golden rule of diversification.

We should all take a moment to consider how much of our money is in these tech stocks. Here’s a specific example. I own the iShares MSCI World exchange-traded fund. It’s the ultimate lazy and cheap way to invest in 1,300 of the world’s largest companies in one product for 0.2% a year. Brilliant.

But 5.5% of this is in Nvidia. 4.6% in Apple, 4.5% in Microsoft and 2.6% in Amazon. Add Meta to the mix and about 20% of this global fund is in 5 companies. I don’t want more than 5% of my total savings in one company, ultimately vulnerable to the performance of one man, Nvidia CEO Jensen Huang. That’s not about P&Ls or economics. It’s just basic risk management.

So, I’m trimming the sails a little, keeping some cash for shorter-term goals and investing a little more in other sectors and regions. Without doing anything too dramatic. We want to enjoy the AI revolution, not be beheaded by it.

The killer question

There is one question I periodically ask myself and this is the most important question any investor should have. If stock markets were to fall by say 30% at some stage over the next 12 months, would I need to be a forced seller? In other words, would I need the money so be forced to sell at rubbish, low prices? If the answer is ‘Yes’, then do something about it now to remove this risk. If the answer is ‘No’, then you will be fine.

When a correction comes (as it will – they always do and that’s fine and normal) I suspect it will be quicker to fall than before. First, because social media today fans every bad news flame. Take a second to consider the impact of the Financial Crisis in 2008 if X and Reddit had existed then – I think it would have been worse. And second because retail investors are moving markets in a way they have never done before because there are more of them than ever. When they move, they move fast and they move in packs. There are 13 million DIY investment accounts in the UK and nearly 2 million were opened in the first 9 months of this year alone. A lot of investors have never seen anything other than a sustained bull run with the odd blip.

For those interested in understanding more about diversification, this week we’ve a new piece on healthcare, a reader question from a cautious 70-year-old on how to invest, and our round-up of the best-selling funds and trusts of October 2025.

Some final news on cash

Cash is also an important ingredient in everyone’s financial larder, and this week we learned that the ‘FSCS’ compensation limit will be increased to £120,000 from 1 December. In other words, you can have up to this much in savings with a UK-authorised bank or building society and get up to £120,000 in compensation if they go out of business – per person and per firm.

A lesser-known fact is that they will also cover temporary high balances of up to £1.4 million for 6 months after a life-event such as selling a home or receiving an inheritance.

Over and out for this week. I’m heading for a swim in the sea to cool my brain as we get ready for a pretty massive money week next week. See you then.

Holly

Post a comment:

This is an open discussion and does not represent the views of Boring Money. We want our communities to be welcoming and helpful. Spam, personal attacks and offensive language will not be tolerated. Posts may be deleted and repeat offenders blocked at our discretion.