Active vs Passive Ready-Made Portfolios - The Performance Data Speaks

Written by Boring Money

10 Mar, 2026

This section is a paid promotion created in partnership with Quilter Invest. The views and information presented reflect the sponsor’s messaging and may not represent the independent opinions of Boring Money. While we aim to ensure accuracy and relevance, this content should not be considered impartial advice.

Not all passive portfolios are created equal. Boring Money's analysis of 30+ ready-made portfolios looks at what investors actually earned over five years — and finds that the choice of provider matters far more than most people realise.

The active versus passive debate often feels theoretical - higher fees versus lower costs, human expertise versus index tracking. In reality, the company you choose and its approach is more important than whether you choose an active or passive solution.

Passive can't mean inactive: investors need to be diversified geographically and rebalance regularly. This helps achieve consistency. Passives are simply the building blocks for an active approach.

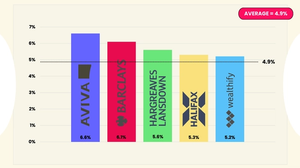

The £1,000 Test - Making Performance Real

Boring Money’s Q4 2025 analysis of 30+ ready-made portfolios reveals what actually happened to investors' money over five years, converting percentages to the return on a £1,000 investment. One provider's passive approach consistently ranks in the top three across all risk categories.

The Real Cost of Choosing Wrong

Over 5 years, Quilter's passive high-risk portfolio delivered 70.1% returns vs Charles Stanley's active Multi-Asset Adventurous at 33.0% - that's an extra £371 on every £1,000 invested.

One strong fund could be luck. An investment manager may have leaned heavily into the artificial intelligence trade, for example, or it could be that a group has particularly strong expertise in a single area. When selecting a multi-asset provider, investors need to see consistency across a range of different objectives and across multiple time frames.

Most providers excel in one category but falter in others. Barclays Growth leads medium risk over five years but sits mid-table elsewhere. Moneybox shows strength in some long-term high risk metrics but struggles on short-term and low risk.

Quilter's performance is unusual for its consistency across every risk level. Its high, medium and low risk strategies have all performed ahead of their peer group over the short term (one year) and the long term (five years). Quilter's top-tier performance across the board suggests robust methodology, not lucky timing.

Quilter's MyGoal range is available to invest in directly. Boring Money readers can access a 40% platform fee reduction — use code NEWYEAR26 when you invest. Find out more.

Five Decades of Learning: How Heritage Shapes Modern Portfolio Strategy

The Quilter MyGoal range was launched in 2013 as a basic risk targeted solution for clients who were happy to give up the potential to achieve greater active returns in favour of simplicity and lower costs.

Our approach is disciplined. We invest based on fundamentals, not hype – and diversification, especially when global equity indices are so concentrated. Our view is that a well-diversified portfolio remains the best defence against uncertainty, helping investors capture upside potential while protecting against inflation, inevitable market corrections, and shifting global sentiment.

In 2026, for example, there are reasons to believe that financial market returns are likely to be well supported, but there are a range of risks: a new chair of the Federal Reserve in the US could change the central bank’s approach, market concentration is rising, and the possibility of an asset bubble is increasing. We believe these are risks that need to be managed carefully.

We believe that diversification matters more today than at any point in recent history. It is easy to believe that an index that represents the whole of the global equity market is well-diversified. However, the index may have become increasingly top heavy and concentrated. The MSCI ACWI index, for example, has almost 5% in one company, Nvidia, and the top 10 stocks (all of which are tech related companies) represent 23% of the index. That’s 10 companies representing 23% of the whole world’s market capitalisation (of large and mid-cap companies).

Meanwhile, the US accounts for more than 60% of the index, so if you are a non-US investor, you are betting a lot not just on the US stock market but also on the US dollar. The index is increasingly looking like a high conviction active portfolio, but without anyone doing the investment due diligence. They are simply relying on the (unreliable) wisdom of the crowd.

We think carefully about the regions to which we want to allocate our clients’ capital, plus the size of the allocation required to mitigate the risks that have built up in these increasingly concentrated indices.

Ultimately, there’s no such thing as a passive multi asset portfolio. Investors have to make active asset allocation decisions. Even if you only wanted to invest in the ACWI index and a bond index, say Global Aggregate, you still need to work out your weighting between the two, and 60/40 probably isn’t the right answer. Therefore, a rigorous asset allocation process that is reviewed with appropriate frequency is absolutely vital.

Inside the Strategy: A Fund Manager's Perspective

2025 was an eventful year for markets, and the MyGoal passive range navigated it with some notable tailwinds — among them a well-timed UK equity allocation and a diversified approach that benefited when European markets outpaced global peers in the final quarter. We spoke with Marcus Brookes, Chief Investment Officer, Quilter, about the thinking behind those positions, how the portfolios are managed day to day, and what investors should bear in mind heading into 2026.

Strategic Asset Allocation

❓The 25% UK weighting in Adventurous caught the FTSE 100's 25.8% return - walk us through that decision.

UK domestic equities are regarded as less risky for UK investors given they are priced in sterling. Of course, there is currency risk in the earnings of these companies – around three-quarters of FTSE 100 earnings come from overseas – but at least the share prices themselves aren’t directly affected by swings in currencies. This is part of the reason our optimised strategic asset allocation (SAA) likes to allocate to the UK.

The UK bias in most of the portfolios has reduced a bit in recent years, in line with where we foresee the best return opportunities. Adventurous is an exception – it used to be ex-UK, so it could get up to the appropriate amount of volatility. Having more US and less UK was a fantastic trade over the past decade, but when we updated the SAA in 2024, we added the UK back in. We preferred to have the portfolio running with a bit less volatility (but still within the Adventurous band), but to be more diversified, given stretched valuations in the US and risks that we could see brewing relating to US index concentration. Put most simply, the US had a good run, so the prudent move was to take some chips off the table.

As much as we can try to predict the future, we really don’t know what will happen, so spreading our bets is a vastly more sensible strategy than putting all our eggs in one basket. We may not be the top performing fund in the short term – there will always be someone who guessed right and had all their equity exposure in, say, South Korea last year, but that doesn’t give you many paths to victory in an uncertain world. Over the long-term, we want to give ourselves as many ways to win as possible.

Geographic Diversification

❓Q4 saw MSCI Europe ex UK return double the MSCI World - was this deliberate or your strategy working as designed?

Our strategic asset allocation is reviewed quarterly and typically updated annually, most recently at the end of September. We did not reposition the portfolios specifically because we had a short-term positive outlook for European equities, but we did increase the Europe weight at the SAA update, so that proved to be well timed.

❓How do you position for market rotations?

We think long term. Our passive range does not have tactical asset allocation. So our focus on the 10y return and risk forecasts, as well as the correlation between assets, to deliver a diversified portfolio that can perform in many scenarios, be they continuations of the status quo or market rotations.

The Rebalancing Advantage

❓How frequently do you rebalance MyGoal portfolios?

Over the medium to long term, markets typically trend up or down (usually up), but day-to-day, the moves are essentially random. This means that in sideways markets, you can pick up a rebalancing return by selling winners to lock in profits and topping up losers to take advantage of price weakness. This return is difficult to attribute accurately, but it is very much real. You do have to consider trading costs – very tiny trades aren’t worthwhile.

We also rebalance relatively daily, so we don’t inadvertently become overexposed to an asset class or region that has done well recently (and might be due a pull back).

Passive Implementation, Active Thinking

❓You use passive funds but make active allocation decisions - explain this hybrid approach

Any allocation decision is necessarily active, but we don’t chop around the portfolios on a short-term basis. The SAA is the bedrock of returns and is the most important factor dictating how your portfolio will perform.

❓What role does fund selection play within passive implementation?

Very important and often overlooked. Different fund providers are better at different things. Tax efficiency needs to be considered, too. A great example is our holding in the Amundi Core MSCI Emerging Markets Swap ETF. By holding a swap ETF rather than a physical ETF, you avoid capital gains tax on Indian and Brazilian stocks, and at times, you can also be paid extra to be long Chinese stocks (because there is excess demand from hedge funds to short them). This delivers consistent and repeatable outperformance vs a physically replicated ETF or index fund.

The passive range doesn’t do short-term tactical trades. We also only have exposure to regional cap weighted indices – no MSCI USA Value, for example. This means we do not strive to profit from rotations within regions. This means we have not been responding to the recent volatility in the technology sector, for example.

That said, we remain well diversified. Around 35% of our equity exposure is in the US compared to nearly double that in the MSCI ACWI, so we are well placed to capitalise on US underperformance should it continue.

❓What is your advice for investors choosing between active and passive?

Passive is clearly in vogue and has had a lot of tailwinds in recent years, but many indices increasingly look like high conviction active portfolios. This is OK, but investors need to go in with their eyes open and understand the risks - the US index doesn’t offer the same sort of diversification that it used to, with returns very dependent on mega cap tech. This can be partly mitigated through regional and asset class diversification, but active managers can help you go even further.

Most passives are just equities and bonds. We also have alternatives (and cash) in our passive funds to protect better even when bonds don’t – like in 2022.

Passive doesn’t just mean set and forget. Different providers have different degrees of rigor they place on asset allocation and fund selection. It’s important to pick a good provider and not assume that there isn’t a lot of difference between passive options.

Ultimately, active or blended portfolios should outperform in the long run, but can have long periods where they don’t. That doesn’t mean active is broken forever, you just have to be patient But as with passive multi asset, for active you’ve got to pick someone good.

Beyond Low Fees - What Actually Works

Passive portfolios benefit from lower fees, and this can be an important factor in driving long-term returns, but it is not enough by itself. All Boring Money data is net of fees – it shows what investors actually received. Fee savings compound, but smart allocation drives the real outperformance.

Quilter's success is driven by more than simply fee savings. There were a range of incremental strategic decisions that paid off for its investors. For example, the MyGoal - Moderate portfolio had a 67% equity

weighting versus a range of 51-54% for its competitors. This helped maximise performance in a ‘risk on’ year for global financial markets. A strategic shift into European equities in the middle of the year captured the rotation into Europe in the fourth quarter - Europe ex UK returns were double that of the World index.Quilter also operates disciplined rebalancing. This helps ensure portfolios remain in line with their targets, captures gains, but also buys into weakness.

The numbers prove the success of Quilter’s approach. This isn't a ‘set and forget’ passive option, with all the risks that entails. It is using passive funds to implement active asset allocation decisions.

Why This Matters for 2026

With the end of the tax year deadline approaching, investors are choosing ready-made solutions for their ISAs and SIPPs today. At the same time, the market is in flux. With investors increasingly wary of the high valuations on US technology stocks, they are rotating away in search of alternative sources of growth.

It is an unpredictable moment in global stock markets, and the buy and hold passive strategies that have worked well over the past five years may not be as successful looking forward. Investors need to ensure that their ready-made solution can adapt to a shifting environment and accommodate changes in market leadership.

At Boring Money, we suggest investors look for three to five yeartrack records, not just last year's winners. Performance across multiple risk levels can demonstrate that an investment group has a robust methodology, rather than just being lucky. Geographic diversification matters in uncertain markets, along with the ability to adapt to changing environments.

If you're reviewing your ISA ahead of the tax year end, Quilter's MyGoal range is worth a look. Use code NEWYEAR26 for a 40% platform fee reduction. Explore the MyGoal range.

Conclusion

Passive investing has advantages. However, it is not a panacea. Passive investing requires a disciplined and strategic approach that can deliver over multiple risk levels and time frames. Quilter’s MyGoal range has stood the test of time.

Strategic allocation combined with cost efficiency gives investors the best of both worlds - experienced decision-making without the fee drag.