He's baaaaaack

By Holly Mackay, Founder & CEO

8 Nov, 2024

Over the last week we’ve been digesting the impact of the Budget, witnessing a new Tory leader, seeing the astonishing return of The Flumps to the White House, watching a new all-time high in the US stock market AND learning of a 0.25% cut in interest rates. A quiet week really.

On Wednesday, as I watched the horrendous sight of that baboon-bottom mouth making triumphant shapes and noises, the US stock market rose to new heights. What does Trump mean for markets? The belief is he will cut red tape, remove some regulatory risk for tech stocks, love the banks, massage Musk hence Tesla, drill baby drill and be generally pro-business. There is also a strong likelihood of hardcore tariffs which will likely boost inflation as prices probably rise.

Higher inflation means higher interest rates for longer and the UK is not immune to these shifts in the US. Couple Trump’s inflationary motorcade with last week’s Budget here, which had massive borrowing plans which have freaked out investors, and ‘yields’ (like interest rates) on 10 year Government bonds hit a 12-month high. This may sound good, but it actually means that the price of these bonds is falling as people think the UK looks like a bit of a dodgy long-term bet compared to other markets.

It also means we're likely to see interest rates stay higher for longer. It may even be that some lenders raise mortgage rates as soon as next week. Overall, pundits don’t expect a big rise in borrowing costs, but we can expect to see rates fall at a slower rate than we anticipated. The base rate fell to 4.75% this week and the odds are no longer backing another cut in December.

The Budget - Your actions and reactions

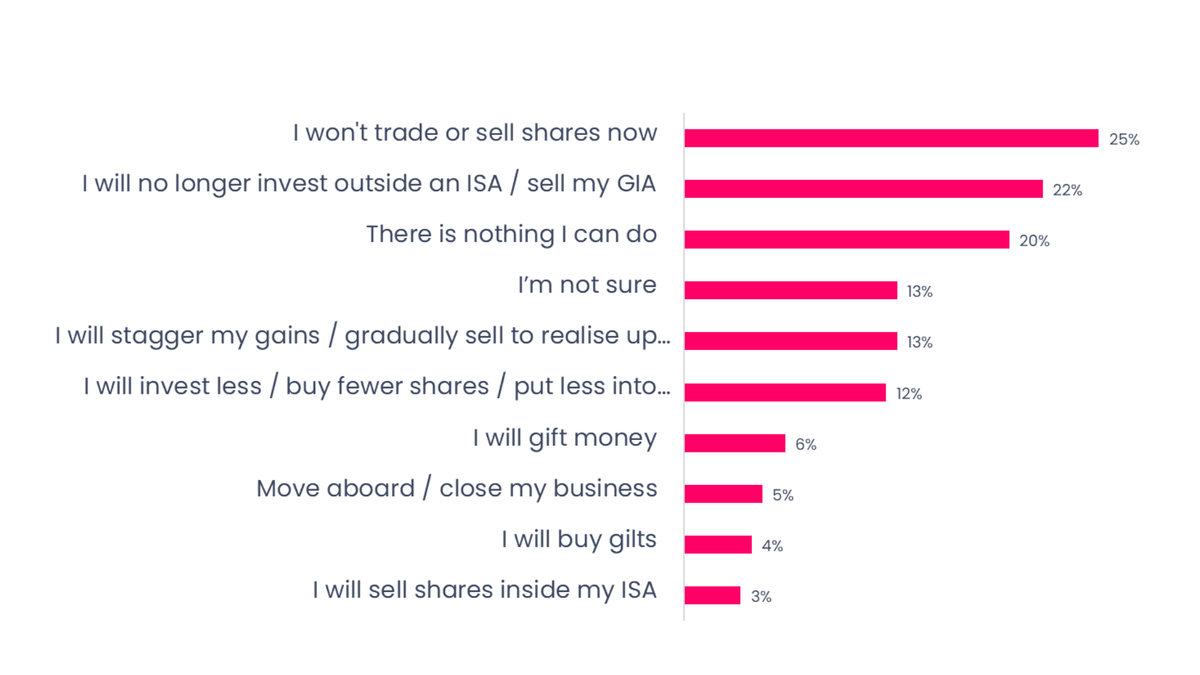

Last week we asked what your reactions to the Budget were and how this had changed your plans. Thanks so much to everyone who responded. You can see below how you told us you're planning to react.

Boring Money Reader Survey. Base 645 completed responses

The main gripe was about pensions being included in Inheritance Tax (IHT), which had many of you spitting chips, to use a brilliant Aussie expression. I imagine we will see a jump in gifting as a result (remember the 7 year rule), some people will just think 'stuff it' and spend more and others will consider other moves, such as using up a pension earlier or using the money to pay into a child’s pension which would be exempt from recycling rules and is very tax-efficient.

Adult readers with older parents – ask for a pension contribution for Christmas?! Normally, third-party contributions into a child’s pension are treated as if the child has made the contributions themselves. This would mean you receive 20% tax relief from the government when the parent pays in and could be entitled to 40% or 45% tax relief if you're a higher-rate or additional-rate taxpayer.

If not already married, pension holders might consider this (ain’t romance great?!) and pass your pension to a spouse with no IHT. However, pensions and estate planning is complicated stuff and getting it wrong can be expensive – I would suggest taking financial advice.

Annuity – Stick or twist?

One beneficiary of higher rates for longer are annuities. These are one option for your retirement income (the other option is a ‘drawdown’ pension). With an annuity, you effectively take a chunk of your pension money (can be some of it, not all) and swap it now in return for a known income stream every year. The government-backed Money Helper has an annuity calculator so you can have a play and see what you could get.

According to Hargreaves Lansdown, this week, a 65-year-old with a £100,000 pension can currently trade it in and get £7,499 per year from a single life level annuity. This is the highest we’ve seen since November 2022.

Some people mix and match, taking the certain income stream from an annuity, while leaving some in a pension drawdown account to dip into as and when needed. I think of these options a bit like ‘Stick’ or ‘Twist’ in pontoon. Annuities are saying, “Stick, it’s 17, that’s good enough, I want certainty”. And drawdown is like saying, “I think overall I could do better, but there will be some gain and some pain and uncertainty along the way”.

Buckle in for the ride

As the dust settles on a pretty momentous week, I think one thing we can predict with some certainty is volatility. Valuations in the States were already high. Markets are nervous. Geopolitics could loosely be described as a tinderbox. If you’re after certainty and have short-term timeframes (under a year or two), remember that you can still get around 4.8% in a one year fixed bond. Stock markets should always be a longer-term play. That said, on the other side of the coin, for longer-term savings, it’s impossible to time the markets. I might be tempted to trim a few positions, but in general, I will carry on, in my own boring way, but expect to see volatility.

Have a good weekend everyone. I am hoping and dreaming that the terrifying Mr Musk will soon finish his nice rocket to Mars and stuff it full of Trump, Putin, Kim Jong Un, additional National Insurance payments, brussels sprouts, the colour brown and goats! Bye bye, Elon...

Holly

Want to get Holly's weekly blog straight to your inbox?

Already have an account? Login